DECISION

Introduction

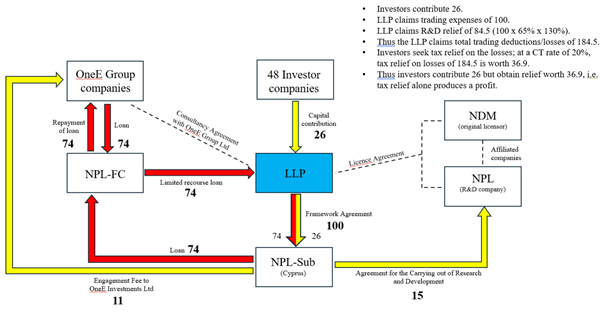

1. The Appellant, L R R&D LLP (the "LLP"), appeals against closure notices issued by HM Revenue and Customs ("HMRC") which disallowed partnership losses totalling £14,715,954 (comprising £3,656,741 in 2014-15, £11,055,590 in 2015-16 and £3,623 in 2016-17).

2. HMRC contend that the LLP's losses arose pursuant to a tax avoidance scheme in which the LLP was used to deliver the scheme's purported benefits, ie creating losses which could then be claimed by the members of the LLP to set off against other income.

3. The LLP contends that, although the arrangements concerned involve a number of agreements and several different parties (as described below), it is, in essence, entitled to claim the losses which arise from expenditure it incurred under an agreement, dated 25 March 2015, that it entered into with NPL Sub-Contractor Limited ("NPL-Sub"), described as a research and development framework agreement (the "Framework Agreement"), for research and development ("R&D") to be undertaken in respect of rights that the LLP had acquired as part of its trade, and that the tax deductible amount was increased on the basis that the expenditure qualified for R&D Relief under Part 13 of the Corporation Tax Act 2009 ("CTA 2009").

4. Although the LLP made a total of £8 million in payments, it accepts that as only £2.9 million of R&D has actually been delivered, any claim for relief should be restricted accordingly.

5. Rory Mullan KC appeared for the LLP. HMRC was represented by Imran Afzal, Harry Winter and Riya Bhatt. We have been greatly assisted by their submissions, both written and oral. Although we have taken all of them into account, we have not found it necessary to make specific reference in our decision to all of the submissions, materials or authorities to which we were referred.

Evidence

6. In addition to an electronic hearing bundle comprising 3,890 pages, we heard from Dr Fazlul Chowdhury and Mr Bashir Timol who gave evidence for the LLP. No witnesses were called for HMRC.

7. Dr Chowdhury described himself as a "technologist", someone who looks for problems and finds technological and scientific solutions to them. He is the Chief Executive Officer ("CEO") of Nemaura Pharma Limited ("NPL"), a private pharmaceutical company, for which, in addition to being its chief scientist and innovator, he deals with licensing, partnerships and inward investments. Dr Chowdhury is also CEO of Nemaura Medical Inc ("NM"), a company incorporated in Nevada, USA and publicly listed on the Nasdaq stock exchange. He has around 130 patents across multiple platforms.

8. Mr Timol, although not a scientist or tax adviser, has, he said, "experienced success in identifying financial opportunities and bringing together people who are specialists in their relevant field to make an entrepreneurial concept into a reality." He is the director of NPL (from January 2007) and OneE Group Limited ("OneE") (from October 2007). OneE provides tax advisory services, particularly in regard to R&D. In addition to NPL and OneE, Mr Timol is a director of a number of other companies in, what he described as, the "tax field". He explained his role at OneE is to "look after the various stakeholders" which includes "keeping them informed and engaged on the R&D which is taking place." He accepted that he was "a controlling mind" of the LLP.

9. Both Dr Chowdhury and Mr Timol were criticised by Mr Winter for inconsistencies in their evidence.

10. In relation to Dr Chowdhury, Mr Winter criticised his reference to an "eightfold return" for investors in the LLP. Other inconsistencies highlighted by Mr Winter included:

(1) Dr Chowdhury's references to the funding of the LLP. In his witness statement he had said that the LLP was only funded to "a certain stage pre-clinical", but orally in evidence claimed that he did not know the extent to which it was funded;

(2) the fact that Dr Chowdhury had said in his witness statement, and confirmed when giving evidence, that NPL had obtained "individual, independent market research for each and every molecule" when that was not the case; and

(3) Dr Chowdhury's claim that there was an outline for the development pathway in the business case, from the beginning of the concept through to the end of development, for "all" of the molecules when there was no such outline for lidocaine, one of the molecules with which this appeal is concerned (the other being risperidone).

11. Mr Winter submits that Mr Timol's inconsistencies in his evidence include:

(1) his references to an "eightfold return" for investors;

(2) what he said in respect of the provision of quotations from third party R&D providers to OneE;

(3) that a "bona fide" benchmarking exercise had been undertaken by NPL rather than NPL-Sub;

(4) his references to the ratio of fees in the £8 million raised by the LLP; and

(5) his acceptance during cross-examination that one purpose of the £8 million payment by the LLP to NPL-Sub was for the LLP to secure tax relief for its investors, something he "corrected" when re-examined when he said that it was the members investing in the LLP that wanted the tax advantage and that the business of the LLP was to "conduct R&D work."

12. Mr Timol also accepted that as an investor in NPL he could "see that argument" when it was put to him (by Mr Winter) that he had "a slightly conflicted position" when he was trying to get the best deal for the LLP while also having a commercial interest in the main or proposed R&D provider.

13. Additionally, Mr Winter contrasted what had been said by Dr Chowdhury and Mr Timol in evidence. For example, in relation to providing quotations to OneE from third party R&D providers, Mr Timol maintained that the process was "bona fide" and "done properly", whereas Dr Chowdhury had said, "it was actually not possible to go out there and get a realistic quotes", explaining, when it was put to him (by Mr Winter) that "the quotes weren't realistic", that "it would not have been possible to go out there and ask somebody to exploit our [NPL's] technology platform without us handing over our IP."

14. Dr Chowdhury had also said that the purpose (not the "only purpose" as Mr Winter submitted) of providing quotes "was to provide evidence to OneE that we were actually competitive and that these were in tune with what the industry norms were in terms of the charges that are levied."

15. Another example of an inconsistency between Dr Chowdhury and Mr Timol to which were referred by Mr Winter was that Dr Chowdhury considered that the drugs [lidocaine and risperidone] at the time they had been selected "could be developed successfully", whereas Mr Timol accepted there was "a high risk of some of the drugs not working out."

16. Notwithstanding this criticism, we found both Dr Chowdhury and Mr Timol to be straightforward and credible witnesses, especially as both had prepared their own witness statements without any assistance. Dr Chowdhury explained that when he was asked to prepare a witness statement nothing had been scripted, he was just told to "[t]ell us what you did." Similarly, Mr Timol said that he was asked to prepare his witness statement setting out his recollections and "that's what I did."

17. We also agree with Mr Mullan that some of the differences between Dr Chowdhury and Mr Timol may have arisen because of the way in which questions were put to them. For example, Mr Winter asked both Dr Chowdhury and Mr Timol about the likelihood of success of the drugs. In relation to Dr Chowdhury the transcript records:

"Q. You are saying that there was a reasonable likelihood that both drugs would be successful; yes?

A. We set out with those drugs with a view that we felt at the time they could be developed successfully, that's correct."

However, Mr Winter put the question differently to Mr Timol, as recorded in the transcript:

"Q. It was extremely unlikely that both drugs would be successful, wasn't it?

A. Yes, there was a high risk of some of the drugs not working out, I accept that, yes."

Approach to Evidence

18. At [15] - [20] in Gestmin SGPS SA v Credit Suisse (UK) Ltd & Anor [2020] 1 CLC 428, Leggatt J (as he then was), in his oft-cited comments on the unreliability and fallibility of the human memory and the adverse effect that the process of civil litigation has on it, said, at [22]:

"In the light of these considerations, the best approach for a judge to adopt in the trial of a commercial case is, in my view, to place little if any reliance at all on witnesses' recollections of what was said in meetings and conversations, and to base factual findings on inferences drawn from the documentary evidence and known or probable facts. This does not mean that oral testimony serves no useful purpose - though its utility is often disproportionate to its length. But its value lies largely, as I see it, in the opportunity which cross-examination affords to subject the documentary record to critical scrutiny and to gauge the personality, motivations and working practices of a witness, rather than in testimony of what the witness recalls of particular conversations and events. Above all, it is important to avoid the fallacy of supposing that, because a witness has confidence in his or her recollection and is honest, evidence based on that recollection provides any reliable guide to the truth."

19. However, in Kogan v Martin & Ors [2019] EWCA Civ 1645 at [88], Floyd LJ, giving the judgment of the Court of Appeal, made it clear that Legatt J's statements in Gestmin was not an "admonition" against placing any reliance at all on the recollections of witnesses and that:

"... a proper awareness of the fallibility of memory does not relieve judges of the task of making findings of fact based upon all of the evidence. Heuristics or mental short cuts are no substitute for this essential judicial function. In particular, where a party's sworn evidence is disbelieved, the court must say why that is; it cannot simply ignore the evidence."

20. Adopting such an approach, we turn to our findings of fact.

Facts

21. NPL was established by Dr Chowdhury in 2005. It is a company that specialises in pharmaceutical research and development and has (in conjunction with the Nemaura Group) has developed and secured a range of pharmaceutical technologies that are pending and/or granted by UK and international patents. Dr Chowdhury, in evidence, said that NPL had the knowledge, skills, ability and capacity to undertake R&D "in house" from the basic concept through to the end product at its laboratories. The only exception to this being "instances" if it does not have a very specialised and specific piece of equipment that is required. In such circumstances, Dr Chowdhury explained, it is necessary to consider whether such equipment should be purchased or an outsource service provider engaged.

22. Dr Chowdhury also explained that, as is standard across the pharmaceutical industry, it was necessary to outsource clinical trials and that it was often a regulatory requirement for a clinical study to be independent of the R&D company.

23. Following a reorganisation of NM, in 2013 NPL was looking for new investors to finance the development of what Dr Chowdhury described as , a "large number of assets" it wanted to exploit commercially. These included the licencing and development of transdermal patch technology to deliver generic drugs. Having previously dealt with Mr Timol and OneE, which had invested in NPL from 2006, Dr Chowdhury turned to them again and was told that they would be able to raise a substantial amount of money through investors using "tried and tested methods" to structure companies in such a way which would benefit the investors. Mr Timol also accepted during cross-examination, although he rowed back from it in re-examination, that one purpose of the payment to NPL-Sub was for the LLP to secure tax relief for its investors.

24. Such arrangements, it was said, would allow NPL to operate and retain ownership and therefore control over its intellectual property and, as Dr Chowdhury explained, allow him to develop the products much faster than if he had to spend time trying to raise external investment and find the right group of investors.

25. The proposed structure was to establish an LLP in respect of a set of molecules, with investors for each LLP. In all, there were 11 LLPs, all of which entered into the same arrangements under which a licence for the exploitation of the transdermal patch technology was granted to the LLP by NDM Technologies Limited ("NDM"). Mr Timol explained, in evidence, that:

"... the whole thing is incentivised by the tax structure, there's no question of that, I'm not denying that. But that can't detract from the underlying substance which is research and development into clinical molecules, into you know medicines. That is the substance of what is happening here, and there's no - to my mind subtracting away from that."

26. It was anticipated that through R&D, the LLPs would develop the rights licenced to them and exploit them for profit. Although the R&D has been successful, the market has changed and neither the LLPs nor NPL has, to date, managed to sell the developed product.

27. The present appeal, as noted above, is that of the LLP and concerns the molecules Lidocaine and Risperidone. It involves a number of contemporaneous agreements (described in greater detail below) that confer rights and obligations on the LLP. Appeals of the ten other LLPs which, although concerning different molecules, are, in factual and legal terms, materially identical to the present appeal and are stood behind it.

Information Memorandum

28. On 5 March 2015, Prosper Capital LLP ("Prosper"), in its capacity as sponsor appointed by the LLP under the terms of the Sponsor and Operator Agreement (see below), issued the Information Memorandum ("IM").

29. After stating its contents should not be treated as "advice", recommending investors "consult an independent financial advisor" and warning of the potential exposure to "significant risk" to a potential investor, that they could lose "some or all of your capital, and potentially more than your capital if you are required to contribute to the losses of the [LLP] pursuant to the Partnership Deed", the IM continues:

"This Information Memorandum is issued by the Sponsor and relates to an opportunity to participate in the [LLP], which is a UK limited liability partnership that has been formed to engage in the trade of exploiting patent rights by undertaking research and development and bringing to market drugs and other pharmaceutical molecules with patented drug delivery technologies. This Information Memorandum sets out the terms on which corporate entities may become members (each a "Member") of the [LLP] (the "Opportunity").

30. The Executive Summary (Part 1) of the IM, under the sub-heading "The technologies", explains how in healthcare, transdermal (into the skin) drug delivery is becoming increasingly accepted as an effective means of painlessly delivering drugs to patients. It also identifies and gives examples of a number of issues with this process.

31. These include:

(1) the limitation on the number of drugs that can be delivered through the skin because of the physical size of the drug molecules;

(2) that larger doses need larger patches which are harder to apply to the skin and therefore to ensure that the correct dose is administered;

(3) that patches use pressure-sensitive adhesives to attach to the skin which in many cases lead to skin irritation and fall off;

(4) that the depth of penetration of the micro-needle will vary from person to person;

(5) that expensive actuators are needed to force the drug into the skin;

(6) that arrays of needles are required to allow the dose to be spread and give rapid absorption of the drug but if one or more of the needles leaks it leads to back flow;

(7) that the pressure across the needles may become uneven leading to inaccurate dosing; and

(8) that multiple needles on an array means the insertion force is spread over the needles needing high forces to ensure all the needles enter the skin.

32. The IM explains that the Nemaura Group, of which NPL is a member, has sought to address these problems by developing patches (the "Patches") using micro-needles to deliver a range of drugs into the skin and that NPL is conducting tests on a number of drugs to assess whether they can be successfully delivered using the Patches. It also describes the benefits of such an approach, and explains that the Nemaura Group has a number of patent rights "granted and pending" covering the Patches and that the core patents covering the technologies has been published in a number of countries including the UK, US, Canada, China and Japan.

33. After stating that further patents covering further aspects of the technology are in earlier stages, the IM continues:

"The Nemaura Group believes there is the potential for a wider range of drugs to be delivered using each of the Patches and has commenced testing on the compatibility of the technologies with a number of drugs. However, each drug will require extensive testing before it can be delivered commercially using a Patch. The Patches may also require customisation to work with different drugs. The Nemaura Group believes that significant research and development funding will therefore be needed to achieve the commercial potential of its Patch technology with a wider range of drugs.

The Nemaura Group has indicated that it is willing to grant patent rights under [the] licence for research and development purposes for the [Patches] in connection with the drugs lidocaine and risperidone. The [LLP] intends to profit from the development of the Patent Rights to deliver the Molecules commercially to patients (the "Venture")."

34. The "Opportunity Review" (Part II) of the IM sets out the proposed arrangements. It states that the LLP is seeking total capital of up to £2,080,000, that members may be admitted by the LLP on a periodic basis and that prospective members are offered the opportunity, subject to the Application Form, to make capital contributions to the LLP of at least £10,000 and up to a maximum of £1 million per member.

35. The "Strategy Overview" explains that the LLP:

"... will, pursuant to a Licence Agreement, obtain the right to exploit the compatibility of the Molecules with the Patent Rights obtained. The Licence Agreement, subject to conclusion of any negotiations, is expected to be entered into on or around 16th March 2015.

36. After summarising the intended agreements to be entered into, the IM, under the sub-heading "Assessment and Success", explains that during the early stages of R&D the LLP will assess the likelihood of Patches being commercially successful, with success being assessed at various stages according to different "milestones" being met. The IM describes how, if the LLP assesses that there is a prospect of success in one or both molecules, ie in this case, lidocaine and risperidone, it may seek to dispose of the technology that had been developed in which case NPL could, at its discretion, exercise its right under the Pre-emption Deed (see below) to acquire that technology from the LLP.

37. If the LLP did not dispose of the technology the Joint Venture Agreement (see below) will provide that the receipts of the exploitation of the technology will be shared between the LLP and NPL and that the LLP will distribute the profit in accordance with the partnership allocations as set out in the Partnership Deed (see below).

38. The IM also explains that testing against a particular molecule may cease if continued testing on that particular molecule is no longer commercially justifiable. It also explains what will happen to the funds and how the third party loan will be repaid.

39. The "Opportunity Overview" section of the IM concludes with an indicative timetable, giving the last application date as 23 June 2015 with a closing date of 26 June 2015. It also sets out the "Application Procedure" for prospective members who are required to remit to the Sponsor, ie Prosper, a completed Application Form, funds representing the relevant capital contribution and anti-money laundering documentation.

40. The next section of the IM (Part III) is headed "Risk Factors".

41. It explains that joining the LLP "involves a high degree of risk" and that it is suitable only for those corporates that "fully understand and are capable" of bearing such risks and warns that only those corporates able to "sustain a total loss to their capital" should apply to join the LLP. The IM also warns that the returns to members will be dependent on the financial performance of patent rights and product with a molecule and that the assumptions and targets included in the IM "are illustrative only and may not be achieved in practice." In addition, it warns that R&D is "inherently risky" and that it is not possible to accurately predict the final value of the product, the fees that can be achieved or the prospect of success of the testing.

42. Under the sub-heading "Innovation risks", it explains that although the LLP in conjunction with NPL has identified the molecules, in this case lidocaine and risperidone, as having the "potential" to be commercially delivered using the Patches there is no guarantee that the venture will succeed and, as has proved to be the case, it might not be possible to achieve a commercially viable product.

43. There is also a warning that as the LLP intends to conduct its business in the competitive pharmaceutical R&D market, it will be subject to "usual market, financial and economic conditions" which may change and, due to circumstances beyond the LLP's control, it might suffer a loss and/or the returns to its members may be adversely affected.

44. In addition, potential members are warned that in order to fully fund the R&D the LLP itself "will be leveraged" with the patent rights and products financed by an element of debt which may rank ahead of any revenues to be paid to members.

45. The "Risk Factor" section of the IM concludes with the following general warning:

"The Venture described in this Information Memorandum is not suitable for everyone. Potential Members must rely on their own examination of the legal, taxation, financial and other consequences of participating, including the risks involved, and must consult their own independent financial advisers, including an adviser authorised under FSMA."

46. In Part IV, the IM sets out the Parties to it and its Advisors. The Sponsor and Operator is Prosper and OneE is the "Asset Arranger". Prosper and OneE are both "Initial Designated Members" of the LLP.

47. The next section of the IM (Part V) "The Company & The Molecules" contains a brief description of NPL and Dr Chowdhury before setting out the background and market research undertaken by Roots Analysis (see below) in relation to the molecules, Lidocaine and Risperidone. This is followed by a "Technical Summary" of those molecules that explains, in broad terms, the areas that need to be considered in relation to skin infusion studies with micro-needles that have been undertaken.

48. Part VI of the IM, "The Partnership", sets out the initial structure of the LLP, how profits and losses are to be allocated as well as describing the LLP's termination. It also explains that once the amounts of the aggregated capital contributions have been calculated, the LLP intends to obtain borrowing, "equivalent to 74% of the total" funds, from a third party lender.

49. Part VII of the IM, "Partnership Activities", explains that the LLP has been established for the purpose of carrying on the "Trade" which it intends to commence as soon as it has been "capitalised, in the manner contemplated" by the IM. It continues by identifying the venture as obtaining the patent rights and bringing to market the product.

50. In terms of R&D, the IM states:

"As the [LLP] itself does not currently have any employees, it expects that it will be necessary to sub-contract the provision of the majority (if not all) of the Research and Development to one or more Sub-Contractors.

In order to provide the necessary commercial certainty that the Research and Development will be undertaken by the [LLP], it is the [LLP's] intention to forward-purchase the necessary Research and Development from the relevant Sub-Contractors under Research and Development Sub-Contracts shortly after entering into the Licence Agreement.

As such, the [LLP] expects to have to pay each Research and Development Sub-Contract price in full to the relevant Sub-Contractor on or shortly after entering into the relevant Research and Development Sub-Contract."

51. This section of the IM concludes with the following table illustrating the projected returns if both Molecules are successful.

|

RESULTS (YEAR) |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

TOTAL |

|

Partnership profit/loss (£m) |

-8 |

0 |

2 |

0 |

4 |

0 |

3.4 |

8.2 |

9.6 |

52. These results are based:

"... on the assumption that the [LLP] raises the Maximum Total Capital and that following the early stages of the testing, [NPL] exercises their pre-emption right to acquire the Developed Technology covering those Molecules and milestone payments are paid by a pharmaceutical company with a view to the pharmaceutical company bringing the Product to market."

53. However, in a preceding paragraph, but on the same page as this table, the IM warns that:

"Financial illustrations and projections contained in this Information Memorandum are for illustrative purposes only. Nothing in this Information Memorandum should be construed so as to constitute a forecast return and none should be implied or inferred. ..."

54. For completeness, we should mention that Part VIII of the IM contains a summary of costs and fees, Part IX summarises the details of the LLP and Partnership Deed (for which see below) and Part X provides details of the LLP's material contracts. The IM concludes, at Part XI, with a glossary of defined terms.

Seminars/Roadshows

55. Once it was completed, the IM was issued to potential investors by OneE. Dr Chowdhury said that these numbered "hundreds, if not thousands" of accountants and contacts representing high-net worth individuals seeking to invest in "these type of opportunities."

56. Dr Chowdhury and representatives of OneE also arranged seminars or "roadshows" across the UK. These were, Dr Chowdhury explained, structured in two halves. The first, presented by OneE representatives was entirely about the tax structure and its operation, albeit with a "health warning" that it was always possible that it might be challenged by HMRC. The other half was based on the technology and was presented by Dr Chowdhury.

57. The presentations explained that each drug would take "around" three years to test and would require "between £2 - £4m of investment depending on the drug". Potential investors were also told that should the drug pass testing, NPL would "acquire the technology from the LLP at around 7 times [the] original investment." The roadshows would conclude with a question and answer session. Dr Chowdhury said that those who attended were extremely engaged, despite the fact that many of them, being business people of all types, did not have a science background.

58. In addition to the roadshows, NPL hosted open days at its laboratories in Loughborough for the prospective investors and their representatives at which further question and answer sessions were held.

Market Research

59. Independent market research reports were commissioned from Roots Analysis Private Limited ("Roots") in relation to 32 drugs (and not "each and every molecule" as Dr Chowdhury said) to identify whether there was a market that justified the R&D being undertaken.

60. Taking the report, received in 2015, in relation to lidocaine, "Lidocaine, Delivery via Microneedles", as an example, its "Executive Summary" explains that Lidocaine is a "local synthetic anaesthetic" and that:

"Topical patches, Lidoderm (Endo Pharmaceuticals) and Synera (Galen US) have been approved for treatment of post herpetic neuralgia and local dermal analgesia respectively."

61. The Executive Summary continues by setting out the "Competitive Landscape" noting that:

"● The primary competition comes from other local anaesthetic drugs such as articaine, bupivacaine, mepivacaine and prilocaine.

● Apart from the competition from other APIs, topical patch (lidoderm patch 5%) also faces stiff competition from several generics that are available in various markets in and outside the US.

● In future, additional competition for lidocaine is likely to come from drugs which are currently under development for topical administration; examples include Fortacin, T2380, PeriZone PerioPatch etc."

62. The Executive Summary then refers to "Current Challenges and Advantages of Microneedle Delivery", observing it is a "well-established challenge" that for the topical patch formulation less amount of drug absorption takes place. Other challenges include the accidental falling off of the patch from the skin and possible allergic reactions. With regard to the "Commercial Potential", the Executive Summary records the decline in sales of lidocaine with an expectation that the market would stabilise by 2030. It also noted that a successful launch of NPL's microneedle product had the potential to capture a "moderate to high share of this market", which in a "particular scenario" at a 35% share NPL could:

"... look to gain ~USD 10 million as upfront payments, ~USD 70 million as milestone payments in addition to royalty payments on future sales."

63. The Lidocaine report also included a section containing a detailed analysis of the benefits of, and approach to, the delivery of drugs via microneedles as well as an "Opportunity Analysis".

64. Material sections of that "Opportunity Analysis" state:

"8.1 Methodology

The approach, outlined below, is based on estimating the valuation (NPV) of a licensing deal for both [NPL] (licensor) and the partner (licensee). The extent of valuation shared between [NPL] and the partner will define the limits for upfront, milestone and royalty payments. However, each of these individually can be flexed to get to the same return for [NPL] under different scenarios.

The NPV of the partner will be primarily hinged on the following two parameters:

1. Incremental Revenue, from delivery of drug via the new technology

2. Costs, which will come in three categories.

a. Pre-launch R&D and marketing

b. Ongoing CoGS, SG&A

c. Payments made to [NPL] (Upfront, Milestone, Royalty)

For [NPL], the NPV is based on the following:

3. Future Revenues, same as Point 2c above

4. Costs, which represents total money already spent on technology development.

...

8.3 Cost Drivers

In order to get the product in the market, additional expenses will be incurred on research & development, gaining market approval, pre-launch marketing etc. We have assumed that NPL's partner will incur 100% of this expense as may be agreed in the terms of the deal. Post launch, ongoing CoGS and SG&A expenses will also have to be considered."

65. The report concludes with the following:

"DISCLAIMER

This report presents work done by analysts at Roots Analysis Private Limited. The views expressed in this report represent independent opinion of the analysts. These views are formed based on extensive business research and are published solely for guidance and information purposes. This report is not a substitute for tailored professional advice. These views shall not be misconstrued as a firm guideline for taking business decisions. We make no warranties as to the accuracy or completeness of information and opinions contained herein. This report may not be sold without the written consent of Roots Analysis."

66. When asked about this, Dr Chowdhury dismissed it as the "standard disclaimer" that any such organisation puts in its reports. However, he was of the view that it would not be "really sensible" to make a business decision solely on the basis the report and that this had not been done in the present case where, as he said in evidence, there were:

"... a whole host of documents, there were discussions, there were lab tours, there were demonstrations, there were a whole host of activities that were undertaken before even we as a company determined that we should pursue certain developments, because ultimately what are we - what was it we wanted after at the end of this? We wanted products to reach market and so that we could generate income."

67. A similar Roots report was obtained in relation to risperidone. The final paragraph of the Executive Summary of that report, which reflected the fact that risperidone is an anti-psychotic drug with a very different market from lidocaine, a local anaesthetic, noted:

"● Due to the unmet need of self-administered injectables (resulting in in high non-compliance), the microneedle based product from [NPL] has the potential to capture moderate / high share of this market. In one particular scenario, at a 35% share of total pre-tax valuation, [NPL] could look to gain between USD 5-10 million as upfront payments, USD 20 - 30 million as milestone payments in addition to royalty payments on future sales."

Agreements

68. There is no issue between the parties that the following agreements were executed by the relevant parties and that some key personnel were involved in more than one agreement.

69. Turning to the various agreements:

Sponsor and Operator Agreement

70. The Sponsor and Operator Agreement was entered into on 5 March 2015 between Prosper, as a person authorised by the FCA to undertake certain functions on behalf of the LLP, OneE and the LLP. As noted above, the LLP appointed Prosper, under this Agreement, to act as sponsor of the IM and operator of the LLP, and to provide or procure the provision of the services set out in Schedule 1.

71. The Sponsor Services included reviewing and issuing the IM, and the Operator Services included arranging the preparation of the LLP's accounts and maintaining or procuring the maintenance of a register of the interests of members in the LLP. There was to be a Sponsor of £11,500 plus VAT on the date of each Partnership Close (the final date in a calendar month on which members would be admitted to the LLP), and it was intended that there would be monthly Partnership Closes until the LLP was fully funded. The Operator Fee was a sum equal to 1.25% of the distributable profits of the LLP after the LLP's tax liability due on each anniversary of the Partnership Close until the LLP was wound up. The Operator services included an obligation on Prosper to:

"Maintain or cause to be maintained for the purposes of any obligations under FSMA the [LLP's] records and books of account and procure that such records and books of account are maintained to reflect the activities of the [LLP]."

LLP Partnership Deed

72. The parties to the Partnership Deed, dated 23 March 2015, are OneE (as the "First Founding Member"), Prosper (as the "Second Founding Member") and the LLP (as "the Partnership"). Mr Mullan described many of the clauses in the Deed as "boiler plates" and, as such, these are not set out below. However, it is necessary, as part of the context and background to the arrangements entered into by the LLP to refer to several clauses of the Partnership Deed.

73. Various definitions are contained in Clause 1. These definitions include:

""Designated Members" means those Members who are from time to time designated for the purposes of section 8 of the [Limited Liability Partnership Act 2000] in accordance with Clause 7.1 (Number and identity of Designated Members).

"Drug" means a particular drug or medication in relation to which the Partnership has obtained a licence to exploit the TDP Technology as a means of delivery for.

"Fundraising Accounting Period" means an Accounting Period

(a) during which an Introducing Subscribing Member makes a capital contribution to the Partnership; and

(b) which is designated as such by a Designated Members' Decision issued by the Designated Members.

"Know-How" means the unpatented technical and other information relating to the TDP Technology and which is not in the public domain regardless of how such information is collected or recorded, and whether protected by copyright, design rights or otherwise and including without limitation, all inventions, data, designs, formulae, compounds, methods, models, assays, research plans, procedures, results of experimentation and testing (including results of research and development) data analyses, reports and information contained in any submission to ethical committees and regulatory authorities.

"Introducing Subscribing Member" means in respect of any single Accounting Period a Subscribing Member who makes a capital contribution in that Accounting Period under agreement with the Designated Members, of not less than £10,000.

"R&D Agreement" means any agreement for the provision of research and development services in connection with the use of TDP Technology as a means of delivering a drug to the bloodstream of a patient.

"Subscribing Member" means all persons who are admitted to the Partnership as a Subscribing Member

"TDP Technology" means the transdermal patch technology for delivery of medications to the bloodstream of a patient, the Know-How and the patents and patent applications relating to it, ..."

74. Clause 2 provides that the LLP is subject to regulation and requires an Operator to establish, operate and in due course wind up the LLP.

75. The nature and purpose of the LLP is set out at Clause 3. The material parts of Clause 3.2, headed "Purpose" provide:

"3.2.1 Without prejudice to the powers (at law or otherwise) of the Partnership to carry on any other business from time to time, the purpose of the Partnership is to carry on the Trade (as defined in Clause 3.2.2).

3.2.2 the Partnerships trade (the "Trade") shall be the exploitation of the TDP Technology with a view to profit and shall include:

3.2.2.1 the acquisition of rights to exploit the TDP Technology in relation to a given Drug under a License Agreement ("acquired rights");

3.2.2.2 the enhancement of the value [of] acquired rights through the carrying out of relevant research and development to ascertain and/or establish the viability of the TDP Technology with a given Drug

3.2.2.3 the sale and/or further licence of the acquired rights; and

3.2.2.4 the engagement by the Partnership in any matter, service or enterprise that is ancillary or related to the Trade, or which the Partnership considers desirable in connection with the Trade

3.2.2.5 the entering into agreements by the Partnership with any other party in pursuance of the above.

76. The number and identity of the "Designated Members" are set out at Clause 7. This provides that at all times no fewer than two Members are Designated Members (Clause 7.1.1) and that the Designated Members shall be, as at the date of the Partnership Deed, the First Founding Member (ie OneE of which Mr Timol is a director) and the Second Founding Member (ie Prosper).

77. Clause 11 of the Deed provides for the allocation of profits and losses. It distinguishes between "Fundraising Accounting Periods", in which an Introducing Subscribing Member made a capital contribution designated as such by the Designated Members, and other "Accounting Periods". In an Accounting Period "other than a Fundraising Accounting Period" Clause 11.1.1.1 provided:

"100% of Net Income, Net Losses, Capital Gains and Capital Losses to the Subscribing Members allocated by reference to their respective Subscription Proportions in the Contribution Period in which the Accounting Period falls."

78. The allocation for a Fundraising Accounting Period, was, as stated in Clause 11.1.2:

"11.1.2.1 As to 0.2% of Net Income, Net Losses, Capital Gains and Capital Losses to the Subscribing Members who are not, in respect of that Fundraising Accounting Period, Introducing Subscribing Members, in proportion to the cumulative total of each such Member's Subscriber Contributions as recorded in the Register of Capital Contributions

11.1.2.2 As to 99.8% of Net Income, Net Losses, Capital Gains and Capital Losses to the Introducing Subscribing Member or Introducing Subscribing Members and, if more than one, in proportion to their respective capital contributions made in that Accounting Period."

Licence Agreement

79. The Licence Agreement between NDM, NPL and the LLP was executed on 23 March 2015.

80. In its recitals, under the heading "Background", it is stated:

(A) NDM is an affiliate of [NPL], and exists as an Intellectual Property Rights holding company for [NPL] and its Affiliates. NDM holds the patented Technology as a means for delivering medications through minimally invasive means.

(B) The viable use of the Technology as a means of delivering the Drugs has not yet been established.

(C) NDM intends to grant the LLP an exclusive licence to exploit the use of the Technology as a means of delivering the Drugs.

(D) [NPL] shall, on behalf of itself and NDM, be responsible for liaising with the LLP on behalf of [NPL], NDM and, if relevant, their Affiliates, and for making any applicable decisions concerning the exercise of its and NDM's rights and obligations under this Agreement.

81. The definitions, contained in Clause 1, include the following:

"Affiliate In relation to any company, a subsidiary of that, company or a holding company of that company (as each such relevant term is defined in the Companies Act 2006) and any other person or entity which is associated to that company. Associated carries the same meaning as the Corporation Tax Act 2010 s 25(4).

Confidential Information: Any and all information and materials of a commercially sensitive or secret nature, in whatever form, whether tangible or intangible, including any copies, and whether disclosed before or after this Agreement, which is now or at any time after the date of this Agreement owned or controlled by one party, including all summary reports and analyses made by any party or their respective advisors which contain or reflect such information notwithstanding the information is owned or confidential to a third party, whether technical, commercial, financial or otherwise, relating to that party and/or its products, intellectual property rights, business or marketing activities, and which is marked confidential and/or from the circumstances in which it is made available to the other party the information ought to be treated as confidential.

Completion of Research: Either (i) all of the research specified in Appendix 2 has been carried out in relation to that Drug; or (ii) all such research and development as might reasonably be considered necessary to enable the Technology as it relates to a particular Drug to be lawfully marketed on a commercial basis; or (iii) the R&D Firm has informed the LLP that use of the Technology in relation to that Drug is not commercially viable.

Effective Date: The date of this Agreement.

Drug 1: Lidocaine - local anaesthetic.

Drug 2: Risperidone - atypical antipsychotic.

Drug 3: Porcilis - live attenuated PRRS virus (animal vaccine).

Drug 4: Duramune - multivalent canine vaccine.

Initial Drugs: Drugs 1 to 4.

Drugs: The Initial Drugs and the Supplemental Drugs.

First Pair: Drugs 1 and 2.

Fully Funded: Research and Development is carried out on a "Fully Funded" basis where an R&D Firm:

(a) has contracted to carry out either (i) all that Research and Development specified in Appendix 2 or (ii) all such Research and Development as might reasonably be considered necessary to enable the Technology as it relates to a particular Drug to be lawfully marketed on a commercial basis and

(b) (by the time such Research and Development commences) has been paid by the LLP all undisputed sums due and payable under the R&D Agreement to carry out such Research and Development.

R&D Agreement: An Agreement to be entered into between the LLP and [NPL-Sub] in substantially similar form to the draft Agreement at Appendix 3 (as such terms may be varied by the parties from time to time) or such other written terms as the parties may agree from time to time.

R&D Firm: [NPL-Sub] or any other person or partnership carrying on a business capable of undertaking Research and Development on behalf of the LLP provided that [NPL] has consented in writing (such consent not to be unreasonably withheld or delayed) to the engagement of such person or partnership by the LLP.

Research and

Development Any scientific, technological and/or market research into and/or testing of the Technology as it relates to the Drugs (or any of them) which may include, without limitation,

Research IPR all Intellectual Property Rights generated at any time by or on behalf of the LLP, any R&D Firm or any other sub-licensee in connection with the exercise of the Licence, including any Intellectual Property Rights comprised in or relating to any of the Research Results.

Research Results all technical data, know-how, computer software, notes, chemical compounds, biological material, models, prototypes, specimens, drawings, reports, and information, all documents concerning regulatory submissions and Marketing Authorisations and any improvements to the Technology, generated at any time by or on behalf of the LLP, any R&D Firm or any other sub-licensee in connection with any Research and Development.

Second Pair: Drugs 3 and 4.

Supplemental Drugs: Those four medications and/or drugs which are determined in accordance with Clause 6.

Technology: The transdermal patch technology ... which enables the delivery of medications to the bloodstream of a patient through minimally invasive means and any developments and/or improvements to it developed by or on behalf of NDM and or [NPL] (or any Affiliate of either of them) including the Know How, the Patents and all other Intellectual Property Rights of NDM and/or [NPL] (or any Affiliate of either of them) in any of the foregoing, whether existing at the Effective Date or which come into existence thereafter.

82. Clause 2.1 provides:

"In consideration of the matters set out below (and in particular the benefits to NDM and [NPL] of the Research and Development, and assignment to NDM of the Research IPR and Research Results), NDM hereby grants to the LLP, with effect from the Effective Date, an exclusive royalty-free licence under the Technology to exercise all and any of NDM's rights and privileges anywhere in the world in and to the Technology insofar as it related to each of the Drugs (the "Licence").

83. Under Clause 2.2, NDM (and if applicable) NPL are required, on the written request of the LLP, to make available at no cost to the LLP, "all such documents, records, samples, materials and/or other Know How relating to the Technology ... as are reasonably necessary or desirable" to carry out R&D and/or for the commercial exploitation of the transdermal patch technology. This right has not been exercised by the LLP.

84. Clause 2.3 provides that, without prejudice to the generality of Clause 2.1, the rights granted to the LLP include the use of the Technology insofar as it relates to any of the Drugs (clause 2.3.1), to sub-licence the rights under Clause 2.1 to the R&D Firm (clause 2.3.2) and to manufacture (or procure the manufacture of), dispose of, offer for sale or disposal to any person or evaluate any product which involves the use of the Technology insofar as it relates to any of the Drugs.

85. The parties were also able, pursuant to Clause 2.5, to agree to substitute any one of the Drugs for a different drug.

86. Clause 3 provides:

"3 Research into the Drugs

3.1 The LLP shall, at its own expense, engage the R&D Firm to undertake Research and Development up to Completion of Research to determine the viability of the use of the Technology in relation to each of the Drugs on the terms of the R&D Agreement [ie the Framework Agreement - see below].

3.2 The LLP shall ensure that, within 12 months of the Effective Date, the R&D Firm will have commenced (or procured the commencement of) Research and Development in relation to the use of Technology as it relates to the First Pair, and that such Research and Development shall be carried out on a Fully Funded basis.

3.3 The LLP shall ensure that, within 12 months of Completion of Research in relation to both the First Pair, the R&D Firm will have commenced Research and Development in relation to the use of the Technology as it relates to the Second Pair.

3.4 The LLP will inform [NPL] of the progress of any Research and Development carried out by the R&D Firm from time to time.

3.5 All Research IPR and Research Results shall vest in and be owned absolutely by NDM. The LLP now assigns (and shall precure that each of its sub-licensees, including without limitation the R&D Firm assigns) all of its right, title and interest in and to the Research IPR and Research Results (both present and future) to NDM absolutely.

...

3.8 The parties shall be at liberty to vary or amend (by written agreement) in relation to any Drug the research specified in Appendix 2 to the extent that such becomes necessary or expedient.

3.9 Nothing in this Agreement shall constitute any representation of warranty by the LLP that any Research and Development shall result in any particular outcome.

87. Appendix 2 sets out the areas of scientific and technological uncertainty that require resolution for the transdermal patch technology to succeed in relation to any drug.

Deed of Right of Pre-Emption

88. The Deed of Right of Pre-Emption (or the "Pre-Emption Agreement"), dated 23 March 2015, was entered into between the LLP and NPL.

89. The definitions contained Clause 1, the Interpretation Clause, are in similar terms to those of the other Agreements but also included the following:

"Consideration: The amount payable by [NPL] to the LLP in consideration of [NPL's] acquisition of the Developed Rights following its exercise of the Pre-emption Rights as calculated pursuant to Clause 5.

Disposal The sale, gift, grant, transfer, assignment, novation or any disposal or dealing with the Developed Rights whereby a person other than the LLP would become entitled to all or any of the Developed Rights or any rights deriving therefrom.

Developed Rights: All of the rights which the LLP holds in relation to the Technology as it relates to a Drug, whether such rights exist under the Licence Agreement the R&D Agreement or otherwise.

Pre-emption Event: As defined by Clause 3.

Pre-emption Period: The period of six months after service by the LLP of an Offer Notice on [NPL].

Pre-emption Rights: As defined by Clause 2

90. In addition to defining "Fully Funded" in almost identical terms as in the Licence Agreement (see above), there is also a definition in Clause 1 to "Partly Funded". This provides that R&D:

"... is carried out on a "Partly Funded" basis where the R&D Firm has contracted to carry out Research and Development in relation to the use of the Technology to Deliver a Drug which is not Fully Funded."

91. Under Clause 2.1 the LLP granted NPL the right, following the occurrence of a "Pre-emption Event and at any time during the Pre-emption Period, to acquire the Developed Rights as they related to any Drug which was the subject of a Pre-emption Event, for the Consideration." That right applies to each of the Drugs separately (Clause 2.2).

92. A "Pre-emption Event" is defined by Clause 3. It is only necessary for the purposes of this appeal to refer to Clause 3.1 which provides:

"3.1 If the LLP

3.1.1 receives a genuine offer from a third party to purchase the Developed Rights in relation to one or more Drugs, and the LLP wishes to pursue and/or carry out further investigations and/or negotiations to determine whether or not to make a Disposal of the applicable Drugs on the basis of that offer; or

3.1.2 decides to make a Disposal (as may be evidenced by a letter of intent from the intended purchase if [NPL] so requests) of the Developed Rights in relation to one or more Drugs,

then the LLP shall provide written notice of such occurrence to [NPL], and a "Pre-emption Event" in respect of the affected Drugs shall be deemed to have occurred on the date of such notice."

93. Within five business days of giving notice of a Pre-emption Event, Clause 4.1 requires the LLP had to give NPL an Offer Notice.

94. Clause 5 provides for the Consideration to be paid by NPL to the LLP. Insofar as applicable it provides:

"5.1 If at the date of the Offer Notice either:

5.1.1 all of the research specified in Appendix 2 of the Licence Agreement (or all such research and development as might reasonably be considered necessary to enable the Technology as it relates to the Drug which is the subject of the Offer Notice to be lawfully marketed on a commercial basis) has been carried out in relation to the Drug which is the subject of the Offer Notice; or.

5.1.2 Research and Development is being carried out on a Fully Funded basis in relation to that Drug,

the Consideration for the acquisition of the Developed Rights by Nemaura following its exercise of the Pre-emption Rights shall be the total of the First Cap and the Second Cap.

5.2 Subject to Clause 5.1, if at date off the Offer Notice Research and Development is being carried out in relation to the Drug which is the subject of an Offer Notice on a Partly Funded basis, the Consideration for the acquisition of the Developed Rights by [NPL] following its exercise of the Pre-emption Rights shall be 50% of the Gross Receipts up to:

5.2.1 £100,000; plus

5.2.2 any sums paid by the LLP to the R&D Firm:

(a) in respect of which Research and Development has not been carried out as at the date of the Offer Notice; and

(b) that has not otherwise been refunded to the LLP by the R&D Firm.

5.3 The Consideration ... shall be paid in full by the fifteenth anniversary of the Effective Date ...

5.4 Each Interim Payment shall be calculated as follows:

5.4.1 100% of the Gross Receipts received in the 6 months period to which the relevant Interim Payment relates up to the First Cap; and

5.4.2 once Interim Payments equal to the First Cap have been paid to the LLP, 1/3 of Gross Receipts received in the 6 month period to which the relevant Interim Payment relates to the Second Cap.

5.5 In this Clause, "the First Cap" means:

5.5.1 such amount as is necessary to settle the LLP's liabilities under the Loan Agreement and any Additional Loan;

5.5.2 Plus

(a) if the date of the Offer Notice is before the Second Pair Commencement Date, £2,320,725; or

(b) if the date of the Offer Notice is after the Second Pair Commencement Date, £1,273,150

5.6 In this Clause, "the Second Cap" means:

5.6.1 if the Offer Notice relates to either of the First Pair, the Second Cap shall be £5,137,856 unless [NPL] has already exercised the Pre-emption Rights in relation to the other of the First Pair, in which case the Second Cap shall be £3,419,819;

5.6.2 if the Offer Notice relates to either of the Second Pair, the Second Cap shall be £1,933,720 unless [NPL] has already exercised the Pre-emption Rights in relation to one of the First Pair, in which case the Second Cap shall be £2,761,020;

5.6.3 if the Offer Notice relates to any of the Supplemental Drugs, the Second Cap shall be £1,110,000; or

5.6.4 in the event of simultaneous Offer Notices the Second Cap shall be determined as if Pre-emption Rights had been exercised consecutively in relation to each Drug which is subject to the Offer Notices.

95. Clause 7 makes provision for the failure by NPL to exercise the right of pre-emption either by rejecting an offer contained in an Offer Notice or failing to accept such an offer in which case the pre-emption rights, as they relate to a particular Drug, shall cease and, in such circumstances, it is open to the LLP to dispose of the Developed Rights

96. Clause 8 provides that NPL's right to acquire the Developed Rights in relation to a Drug shall be conditional upon it agreeing that it shall engage the R&D Firm to undertake all such R&D as has been funded by the LLP pursuant to the R&D Agreement which relates to that Drug to the intent that any R&D contracted for and paid for by the LLP in relation to that Drug shall be carried out and that all sums expended by the LLP on R&D in relation to that Drug shall result in a commensurate amount of R&D being undertaken.

Joint Venture Marketing Agreement

97. This Agreement (the "JV Agreement") between NPL and the LLP is dated 23 March 2015 (the "Effective Date"). Its interpretation clause, Clause 1, also contains similar definitions to those seen in the Agreements above, eg Developed Rights, Drug 1, Drug 2 Drug 3 and Drug 4, Technology etc.

98. Clause 2 provides that the agreement shall commence on the Effective Date and continue until 12 months after the latest date on which the LLP enjoyed rights in relation to the Drugs under the Licence Agreement (see above) and would automatically be renewed for a further 12 months unless either of the parties signified their wish to terminate three months before the expiry date.

99. Clause 3, which has the heading, "Sales Strategy", provides:

"3.1 At the request of the LLP [NPL] will draw up a strategy to enable an effective and profitable exploitation of the Technology as it relates to that Drug ("the Sales Strategy").

3.2 The Sales Strategy shall be drawn up in a way which reflects the respective knowledge and expertise of the parties and the respective interests of the parties.

3.3 [NPL] shall have responsibility for implementation of the Sales Strategy.

3.4 [NPL] agrees not to undertake any sales or marketing programme which contravenes the laws of England or any other jurisdiction in which it operates. [NPL] will undertake its sales and marketing business in a legal and decent manner in accordance with the terms of this Agreement and in compliance with any codes of conduct appropriate to the industry.

3.5 The obligations under this clause shall not arise in relation to a Drug if [NPL] acquired the Developed Rights in relation to that Drug pursuant to the Pre-emption Deed.

3.6 If and to the extent that the LLP and/or [NPL] receives or is entitled to receive any amount as the result of exploitation of the Technology as it relates to that Drug, such amount shall be treated as if it were the proceeds of a Sales Strategy whether or not that is in fact the case and shall be shared as provided for in Clause 6."

100. NPL is required, by Clause 4, to act in the "best interests of the parties", to use its best endeavours to obtain the most favourable outcomes for the parties, to keep the LLP informed as to the progress of the Sales Strategy, to provide the LLP with details of all sales, offers and opportunities for exploitation of the Technology. It is also required to provide hard copies of all agreements, a report with details of pending agreements and a report of cancelled agreements to the LLP on a monthly basis (Clause 4.1.5) and provide the LLP with an account of all receipts and expenditure relating to the exploitation as it relates to a Drug (Clause 4.1.6) every six months.

101. Also, unless directed to the contrary, NPL must act in such manner as it considers "to be most beneficial to the LLP's commercial interests and reputation" (Clause 4.1.7).

102. Under Clause 6.1, NPL is to ensure that monies received from the exploitation of the Technology as it related to a given Drug would be paid into a separate account. The costs of implementing the Sales Strategy, and other costs of carrying on the business of marketing the Technology would, pursuant to Clause 6.2, be met from that account. Clause 6.3 provides that the profits were to be shared with 90% to NPL and 10% to the LLP.

103. Although the LLP and NPL entered into this JV Agreement, it was always more likely that NPL would exercise its rights under the Pre-emption rather than rely on the JV Agreement. This is clear from the financial projection in the IM (see above) which was based on the assumption that NPL would exercise its right of pre-emption and the absence of any similar projection in relation to the JV Agreement. Similarly the presentation slides for potential investors referred to NPL acquiring the technology from the LLP, "should the drugs pass testing." It was also consistent with the evidence of Mr Timol that if NPL thought it there was an opportunity to make money it was likely to exercise its pre-emption rights.

LLP Loan Facility

104. Under an agreement, dated 23 March 2015, between the LLP and NPL FC Limited ("NPL-FC"), referred to in the agreement as the "Lender", NPL-FC agreed, under Clause 2.1, to place at the LLP's disposal a loan facility of £5,920,000 (ie the 74% of the total funds referred to in the IM, see above).

105. Clause 3 provides that the purpose of the loan was to fund the R&D that the LLP had contracted for under the R&D Agreement. A covenant in Clause 5.1.1 also restricts the LLP to using the loan "only" to fund R&D which it has agreed to undertake under the Licence Agreement and/or which it has contracted for under the R&D Agreement.

106. There is a further covenant (at Clause 5.1.7) that the LLP will not pay any capital distribution out of the money provided by the loan or an amount up to the amount of the loan "subsisting from time to time" or (at Clause 5.1.8) to make any payment of capital or income to its members until the loan has been repaid in full.

107. Insofar as material, Clause 7 provides:

7. Limited Recourse

7.1 The Loan is only repayable out of Relevant Receipts.

7.2 The Lender's rights of claim as against the LLP and its members are limited from time to time to that amount which is the Relevant Receipts minus the sum of the amounts which have been repaid by the LLP to the Lender; and

7.3 To the extent that the amount which would otherwise be payable under the Loan exceeds the amount to which the Lender has a right of claim under paragraph 7.2 above, the Lender may also have recourse to any rights the LLP has under the Licence Agreement and/or the R&D Agreement [ie the Framework Agreement - see below] for repayment of the Loan.

7.4 In this facility letter "Relevant Receipts" means the Gross Relevant Receipts less Relevant Tax Liabilities.

7.5 "Gross Relevant Receipts" the amount from time to time is the sum total of:

7.5.1 the amount of any proceeds of exploitation of the rights acquired under the Licence Agreement; and/or

7.5.2 any amounts received by the LLP pursuant to the Licence Agreement; and/or

7.5.3 any amounts received by the LLP under the R&D Agreement.

7.6 "Relevant Tax Liabilities" means any liability to tax of any person which arises as a result of the LLP receiving the Gross Relevant Receipts.

108. It is clear from Clause 10, "Interest", that interest, which is chargeable at 7.5% per annum and compounded quarterly (Clause 10.1), is also on a limited recourse basis as Clause 10.2 provides that interest "shall be paid by the LLP at the same time as the principal amount outstanding under the Loan is repaid pursuant to clause 7."

Framework Agreement

109. As confirmed by Mr Timol in evidence, the LLP did not have the capacity, knowledge or workforce (or even the knowledge to hire staff) to undertake the R&D. It therefore entered into the Framework Agreement with NPL-Sub, a company incorporated and registered in the Republic of Cyprus, on 25 March 2015. This Agreement is the R&D Agreement as defined in the above Agreements.

110. It is accepted that, notwithstanding the Recital C in the Framework Agreement stating that NPL-Sub agreed "to perform the services, described in the Task Orders (as defined below) executed by the parties, in accordance with the terms and conditions of this Agreement", that NPL-Sub did not have the resources to undertake any R&D itself but would contract the work out to other parties.

111. Clause 1, the interpretation clause, contains many of the same definitions as in the other Agreements including "Confidential", "Completion of Research", the definition of Drugs 1 to 4 and the references to "Fully Funded", "Licence Agreement", "Research and Development" and "Services".

112. Under Clause 2 the LLP retained NPL-Sub to provide the R&D services in relation to the Drugs as described in Task Orders, a form of which was attached in Schedule 2 of the Agreement (for which see below). However, Clause 2.4 provides that the terms of a Task Order may be amended or modified by mutual written agreement of the NPL-Sub and the LLP.

113. NPL-Sub agreed during the term of each Task Order, under Clause 2.6, to maintain all materials and all other data it generated in the course of providing the relevant services including all electronic records and files (the "Work Product") in a secure area protected from fire, theft and destruction. NPL-Sub also agreed, pursuant to Clause 2.7, to complete the Services by the target date specified in the Task Order with time being of the essence. In the event of failure by NPL-Sub to perform the Services, or any portion of them, in accordance with the date or any later deadline set by the LLP, the LLP could terminate the Agreement and be immediately repaid the total amount of any credit.

114. At Clause 2.9 the parties acknowledged and agreed that by its nature R&D is:

"... speculative and nothing in this Agreement gives any representation that the Research and Development shall deliver any particular results or data."

115. Clause 3.1 required NPL-Sub to commence the Services within three months of receipt of the Initial Payment as agreed in the relevant Task Order.

116. Clause 5 provides for payments by the LLP to NPL-Sub for the provision of Services which was, as Dr Chowdhury confirmed in evidence, the only contribution the LLP could make.

117. Clause 5.1 provides:

"Each Task Order will provide a breakdown of the Research and Development services to be provided together with the fee agreed for this portion of the services to be provided. The cost of delivering the Research and Development (the "R&D Fee") shall be the sum of fees for the services specified in the Task Order and shall be specified in the Task Order."

118. Clause 5.4 makes provision for subsequent payments where the initial fee does not cover the full value of the R&D Fee.

119. Clause 6 provides for changes to the Services if it NPL-Sub reasonably determines that a continuation of the Services is unlikely to result in the profitable exploitation of the rights acquired by the LLP under the Licence Agreement.

120. Subsequent clauses provide for the duration and termination of the Agreement (Clause 7), Credit for unperformed Services (Clause 8), all intellectual property rights being for the benefit of NDM(Clause 9) and a right to assign the rights under the Agreement (Clause 11).

121. Under Clause 14.1 each party undertakes to the other that it shall keep (and procure that its respective directors, employees and contractors to whom it is disclosed) "secret and confidential" the Confidential Information of the other party. However, NPL-Sub is entitled, by Clause 14.3, to disclose Confidential Information to its members, employees or contractors to the extent that it is necessary for the purposes of this Agreement.

122. Schedule 1 to the Agreement provides for the Development Objectives, setting out in some detail (eg stage 2 which considers the need for clinical studies to be undertaken as laboratory models do not bear resemblance to human skin referring to the width and sharpness of a needle, depth of penetration and the likely skin trauma compared to the length of microneedles used the stages of the R&D to be undertaken).

123. Schedule 2 is headed "Task Order Template"

Task Orders

124. The parties to the Task Order are NPL-Sub and the LLP. Its recitals refer to the R&D Agreement, ie the Framework Agreement, which provides for NPL-Sub to provide Services upon payment by the LLP and that the Task Order specifies those Services to be Undertaken by NPL-Sub.

125. The Agreed Terms of the Task Order provide:

"1. In this Task Order, capitalised terms shall have the meanings given to them in the [Framework Agreement] except to the extent specified herein.

2. It is agreed that pursuant to the [Framework Agreement], the LLP shall pay NPL-Sub and Initial Payment of £2,015,385 (being an Instalment of the R&D Fee) upon entering this Task Order.

3. If the Initial Payment is not equal to the R&D Fee, LLP shall pay Instalments up [to] the value of the outstanding value of the R&D Fee in accordance with the [Framework Agreement] and applicable Supplemental Services Agreement.

4. [NPL-Sub] shall deliver the following research and development services in respect of the Initial Pair in order to meet the Development Objectives specified in Schedule 1 of the [Framework Agreement]."

126. Part A sets out the Research Stages. These are repeated in Part B, which is set out in the table below, the "Breakdown of the R&D Fee":

|

Element of the Services |

Cost |

|

Stage 1A: |

|

|

A Formulation Development and Optimisation |

£234,500 |

|

B Analytical Development

C Physical Characterisation |

£234,500 |

|

D Device Development and optimisation |

£201,000 |

|

Stage 1B: Scale-up studies:

· Batch size and process parameter

· Quality by design studies

· In-process control parameter determination

· Quality control methods

· Product release specification

· Packaging compatibility and stability studies |

£165,000 |

|

Stage 1C: Pre-Clinical studies in animal models

· Ethics approvals

· Study design

· Formulation preparation and release

· Device preparation and release

· Product application optimisation

· Bio-analytical method development and validation |

£165,000 |

|

Stage 2A: Clinical Trial Batch Manufacture: Device

· Equipment design and manufacture

· Process design and equipment procurement

· Validation of equipment and process

Stage 2B: Clinical Trial Batch Manufacture: Drug Formulation

· Scale up process development

· In-process testing

· Quality assurance testing and release

· Qualified-person - product release

· Statistical process control |

£900,000

|

|

Stage 2C: First in man studies

· Clinical protocol design

· Ethics approval

· first in man study - 12-20 volunteers

· bio-analytics

· clinical report |

£150,000 |

|

Stage 2D: Long term stability studies

· ICH guidelines on stability testing - to 2 years

· Stability test method development

· Statistical evaluation of stability samples |

£300,000 |

|

Stage 2E: Bridging Clinical Studies in man

· Clinical Studies in man

· Pilot pharmacokinetic studies - 10-12 healthy volunteers

· Volunteer studies - up to 225 patient study

· Ethics approvals

· Clinical study protocol

· Bio-analytical method development

· Statistical analysis |

£1,200,000 |

|

R&D FEE |

£4,000,000 (sic) |

127. The total cost of the services, the R&D Fee, as set out above is actually £3,550,000 not £4,000,000. Mr Mullan referred to this as an "arithmetical error", something that was replicated in the initial Task Order, dated 26 March 2015. Mr Afzal, in contrast, described it as "an error of substance, which then goes to commerciality".

128. However, the total cost, as set out in a summary included in a OneE September 2015 investor update that set out the stages and costs of "the scope of the work expected to be required", did correctly amount to £4 million.

129. This is also the case with regard to an updated Task Order, dated 26 April 2016, giving further details of the various "stages" which had not been included in the earlier Task Order, as described in the above table. These include references to "Analytical method validation" at Stage 1A, "Pharmacokinetic studies - 10-12 healthy volunteers" at Stage 2D and "dossier compilation, chemistry manufacture and controls, clinical data, toxicology data" at Stage 2E.

130. The 26 April 2016 Task Order provides:

|

Element of the Services |

Cost |

|

Stage 1A: The following four areas will run in parallel |

|

|

Formulation Development and Optimisation |

|

|

· Drug Compatibility studies (including preclinical development) |

£35,175 |

|

· Excipient compatibility studies (including preclinical development) |

£35,175 |

|

· Stress Studies |

£35,175 |

|

· Temperature and humidity studies in accordance with ICH guidelines |

£35,175 |

|

· Chemical characterisation |

£93,800 |

|

|

|

|

|

£234,500 |

|

Analytical Development |

|

|

· Excipient characterisation |

£23,450 |

|

· Drug characterisation |

|

|

· Impurity detection and characterisation |

£58,625 |

|

· Solvent detection |

£11,725 |

|

· Residual substance detection |

£11,725 |

|

· Analytical method validation |

£70,350 |

|

|

£175,875 |

|

Physical Characterisation |

|

|

· Solubility |

£58,626 |

|

· Dispersion |

|

· Homogeneity of active pharmaceutical |

|

· Ingredients and crystal seeding/precipitation |

|

|

£58,625 |

|

Device Development and Optimisation |

|

|

· Material selection |

£10,050 |

|

· Material specification determination |

£10,050 |

|

· Material compatibility |

£20,100 |

|

· Device Housing |

£30,150 |

|

· Needle assembly |

£20,100 |

|

· Liquid flow property determination |

£20,100 |

|

· Skin application and ease of insertion |

£20,100 |

|

· Needle insertion forces |

£30,150 |

|

· Skin-needle-drug release inter-relationship |

£20,100 |

|

· Device scale-up |

£20,100 |

|

|

£201,000 |

|

|

|

|

Stage 1B: Scale-up Studies (including Quality by Design Studies) |

|

|

· Batch size and process parameter |

£41,250 |

|

· In-process control parameter determination |

£41,250 |

|

· Quality control methods |

£41,250 |

|

· Product release specification |

£24,750 |

|

· Packaging compatibility studies and stability studies |

£16,500 |

|

|

£165,000 |

|

|

|

|

|

|

|

Stage 1C: Pre-clinical Studies in Animal Models |

|

|

· Ethics approvals |

£8,250 |

|

· Study design |

£8,250 |

|

· Formulation preparation and release |

£41,250 |

|

· Device preparation and release |

£41,250 |

|

· Product application optimisation |

£33,000 |

|

· Bio-analytical method development and validation |

£33,000 |

|

|

£165,000 |

|

|

|

|

Stage 2A: Clinical Batch Manufacture (including Statistical Process Control) |

|

|

· Equipment design and manufacture |

£135,000 |

|

· Process design and equipment procurement |

£90,000 |

|

· Validation of equipment and process |

£135,000 |

|

· Scale-up process development |

£270,000 |

|

· In-process testing |

£135,000 |

|

· Quality assurance testing and release |

£90,000 |

|

· Qualified person - product release |

£45,000 |

|

|

£900,000 |

|

|

|

|

Stage 2B: First in Man Studies |

|

|

· Pilot pharmacokinetics studies |

£300,000 |

|

|

£300,000 |

|

|

|

|

Stage 2C: Long Term Stability Studies |

|

|

· ICH guidelines on stability testing - to 2 years |

£165,000 |

|

· Stability test method development |

£60,000 |

|

· Stability test method validation |

£60,000 |

|

· Statistical evaluation of stability samples |

£15,000 |

|

|

£300,000 |

|

|

|

|

Stage 2D: Clinical Studies in Man |

|

|

· Pharmacokinetic studies - 10-12 healthy volunteers |

£187,500 |

|

· Volunteer studies - up to 225 patient study to cover skin irritation, sensitisation, pharmacokinetics and where appropriate pharmacodynamics and skin toxicology |

£875,000 |

|

· Ethics approvals |

£62,500 |

|

· Clinical study protocol |

£31,250 |

|

· Bio-analytical method development |

£62,500 |

|

· Statistical analysis |

£31,250 |

|

|

£1,250,000 |

|

|

|

|

Stage 2E: Data Evaluation and Analysis |

|

|

· Dossier compilation |

£62,500 |

|

· Chemistry manufacture and controls |

£87,500 |

|

· Clinical data |

£87,500 |

|

· Toxicology data |

£12,500 |

|

|

£250,000 |

|

|

|

|

R&D Fee |

£4,000,000 |