B e f o r e :

Mr Mark Higgin FRICS FIRRV

____________________

| |

EMMA OWEN

|

Appellant

|

| |

- and -

|

|

| |

DAWN BUNYAN

(VALUATION OFFICER)

|

Respondent

|

| |

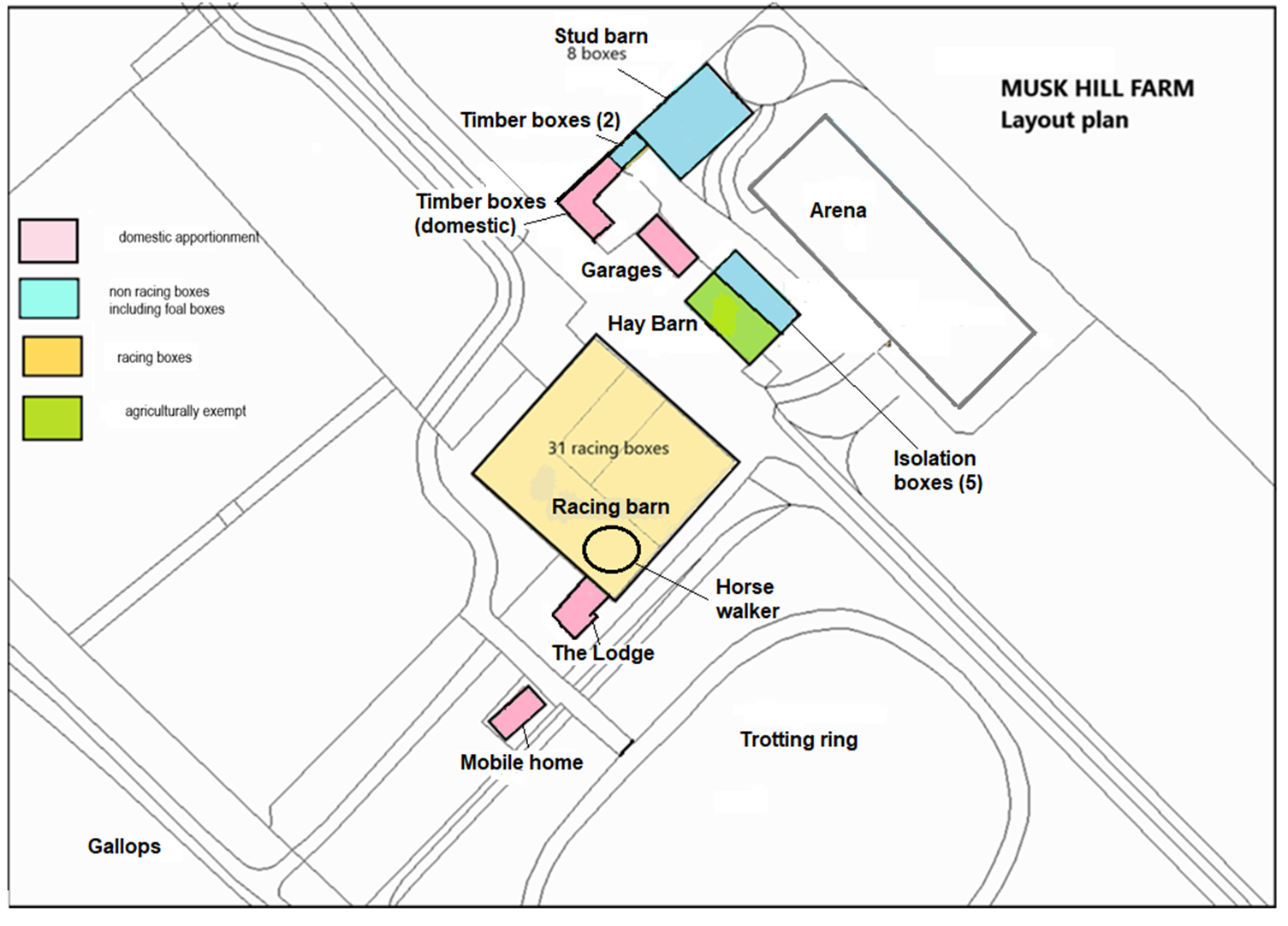

Musk Hill Farm,

Nether Winchendon,

Aylesbury,

Buckinghamshire,

HP18 OEB

|

|

____________________

The appellant represented herself

Ms Isabel McArdle, instructed by HMRC Solicitors' Office, for the respondent

26 November 2024

____________________

HTML VERSION OF JUDGMENT�

____________________

Crown Copyright ©

TRIBUNALS, COURTS AND ENFORCEMENT ACT 2007

RATING PROCEDURE scope of proposal whether information provided at 'check' and 'challenge' stages defines scope of proposal valuation horse racing yard whether works of repair would be economic for a reasonable landlord evidence of other assessments end allowances appeal allowed assessment determined at rateable value £15,600

The following cases were referred to in this decision:

Hobbs v Gidman (VO) [2017] UKUT 63

Joanne Moore (VO) v Caroline Bailey [2024] UKUT 304 (LC)

Midland Bank plc v Lanham (VO) (1977) 246 EG 1117

Nelson Plant Hire Ltd v Bunyan (VO) [2022] UKUT 309 (LC)

Oldschool and Oldschool v Coll (VO) (1994) RA/312/1994

Rozel Motor Company Limited v Clark (VO) (1983) RA 70

Simon Earle Racing Ltd v Virk (VO) [2022] UKUT 311 (LC)

Thomas & Davies (Merthyr Tydfil) Ltd v Denly (VO) [2014] UKUT 146 (LC)

Introduction

- This appeal concerns the 2017 rating list assessment of a horse racing yard (the Property) in Buckinghamshire. It deals with the scope of the proposal that initiated the appeal, the level of value and the impact (if any) of the state of repair of the Property on the valuation.

- The Property was originally assessed in the 2017 Rating List at rateable value £35,250 with effect from 1 April 2017 and in its decision of 2 January 2024 the Valuation Tribunal for England (VTE) reduced the assessment to rateable value £24,250.

- I inspected the Property on 15 November 2024 accompanied by the appellant Ms Emma Owen and her father. Ms Heather King and Mr Roy Albert of the Valuation Office were also present.

- At the hearing Ms Owen represented herself and Ms Isabel McArdle represented the respondent Valuation Officer (VO). I am grateful to them both.

The facts

- Musk Hill Farm is located in rolling countryside about 0.6 miles north west of the village of Nether Winchenden which itself lies 4.5 miles north of Thame and 5.25 miles west of Aylesbury.

- At the material day the Property was being used as a racing yard and stud farm. In all Ms Owen owns and occupies 100.72 acres, split between 60 acres used for the cultivation of haylage and the remainder used for turnout/paddocks and the racing yard. Areas under cultivation and the turnout/paddock areas are classified as agricultural and are exempt from non-domestic rates. The Property was inherited from Ms Owen's former partner, the jockey Mr Patrick Eddery OBE who died in 2015. Mr Eddery's will was contested, and the dispute was unresolved at the material day. A valuation report from May 2016 produced by Carter Jonas in connection with the probate dispute was submitted by Ms Owen in evidence for this appeal. She confirmed at the hearing that permission had been granted by Carter Jonas for this purpose. The report provides a record of the condition of the Property at the date it was written, and I will return to this aspect later in the decision.

- The Property originally operated as a dairy farm and some of the buildings on the site were previously used for that purpose. The main building is a former cowshed, originally of concrete portal frame construction but with a later steel framed addition. The walls are of blockwork and corrugated panels, and the roof is covered in similar corrugated sheets with translucent roof lights. The roof has vents at the ridgeline which are open to the elements and presumably relate to its former function. Currently (and at the material day), the primary purpose of this building is to provide stabling for racehorses and to that end it contains 31 stables or boxes. For the sake of consistency, I will refer in this decision to boxes rather than stables. The boxes have a steel frame with wooden lower parts and steel bars above. They are about 2 metres in overall height. Internally, along the southern wall there are a series of block-built rooms with flat roofs. These are used as stores, an office, and a mess room. The building accommodates a five-bay horse walker (a rotating device for exercising horses) and an area used for baled hay storage. The respondent characterised this building as an 'American barn', a term referring to a particular type of stable building with stables arranged down either side of an open corridor. The traditional style of racing yard has individual boxes set out around a surfaced yard.

- Immediately to the west of the main building is a single storey, timber-built lodge of about 58 m2. This is used by Ms Owen as her sole residence and is entered in the Council Tax List.

- A dilapidated static caravan is located to the west of the lodge, it features in neither the council tax nor rating lists. To the east of the main building, across a concrete yard is an open sided hay store. At the material day it also contained five isolation boxes including one larger foaling box, but these have subsequently been removed. As an agricultural building the hay store is exempt from non-domestic rates. To the north of the hay store are four single storey, brick built garages with 'up and over' doors. These are used for domestic storage and are included in the Council Tax assessment for the lodge. Three timber stables and a tack room with brick and concrete bases which are in poor condition were originally included in the assessment but are now agreed to be domestic. There are two further buildings; a pair of timber boxes one of which is a foaling box, and a stud barn arranged as an American barn and at the material day containing 8 boxes one of which was a foaling box.

- The current assessment contains three additional elements; a post and rail fenced arena measuring 20 metres by 60 metres, a trotting ring of 300 linear metres with a surface of rubber, fleece and sand, and finally a gallop of about 7 furlongs (about 1,300 metres). The gallop is quite steeply inclined with a 50 metre difference in height between the lowest and highest points. All three of these facilities are currently in disrepair to various degrees of severity. I will return to the question of repair and its effect on value later in the decision.

- Ms Owen is licenced by the British Horseracing Authority (BHA) to train 10 horses, but also cares for a number of retired racehorses. She explained that all of the horses at Musk Hill belong to her and are for her personal use. She does not train horses for anyone else and has not done so in the past.

- The Carter Jonas report helpfully sets out the planning history of the property based on information provided by the local planning authority. For the purposes of this appeal it is pertinent to note the following:

i) The static caravan does not have planning permission.

ii) Occupation of the timber lodge is limited to persons solely or mainly working at Muskhill Farm, in connection with the running of the horse stud and training of thorough-bred racehorses. The permission was personal to Mr Eddery and his former wife and when the premises are no longer required for the running of the stud, the building must be removed from the site.

iii) The gallop, trotting ring and walk back track are also subject to a personal condition in favour of Mr Eddery and the former Mrs Eddery and must similarly be removed when they cease to occupy.

Ms Owen also confirmed that a personal condition was attached to the permission for the arena.

- The plan below shows the general arrangement of the farm and the division between the various uses.

- A public footpath runs down the main driveway, through the central part of the yard and then crosses the rest of the Property, running in a north-westerly direction.

The statutory context

- Non-domestic rates are a tax on property and the unit of property which is the subject of tax is the 'hereditament'. Section 64(1) of the Local Government Finance Act 1988 (the 1988 Act), defines a hereditament by reference to the definition in section 115(1) of the General Rate Act 1967, which provided that:

'"hereditament" means property which is or may become liable to a rate, being a unit of such property which is, or would fall to be, shown as a separate item in the valuation list.'

- Schedule 6 of the 1988 Act contains provisions about valuation for the purposes of non-domestic rating. Paragraph 2(1) provides that the rateable value of a hereditament is taken to be equal to the rent at which it might reasonably be expected to let from year to year if let on the material day on certain assumptions.

- The first assumption in paragraph 2(1)(a) is that the tenancy begins on the day by reference to which the determination is to be made. The second assumption, in paragraph 2(1)(b), is that "immediately before the tenancy begins the hereditament is in a state of reasonable repair, but excluding from this assumption any repairs which a reasonable landlord would consider uneconomic". The final assumption, in paragraph 2(1)(c), is that the tenant undertakes to pay all usual tenant's rates and taxes and to bear the cost of the repairs and insurance and the other expenses (if any) necessary to maintain the hereditament in a state to command the agreed rent.

The Parties' arguments

- Ms Owen seeks deletion of the hereditament from the rating list on the basis that the hereditament is domestic. She also says that at the material day the Property was the subject to a dispute and litigation relating to probate following Mr Eddery's death, and that in those circumstances no hypothetical tenant would be prepared to make a rental bid. In her statement of case she submitted that she could not let the property as a racing stable because there was no 24 hour residential accommodation on site and it did not therefore meet the requirements of BHA licencing. In the alternative a further reduction in assessment to rateable value £5,800 is sought.

- The Respondent's position, is that:

a) The VTE correctly excluded the deletion argument from the proceedings, and there is no jurisdiction for the Upper Tribunal to consider the argument.

b) Without prejudice to that primary position, the hereditament is composite with non-domestic parts and should therefore not be deleted from the 2017 Non-Domestic List. The probate litigation is irrelevant.

c) The correct RV is £24,750 if stud relief is inapplicable and £20,000 if stud relief is applied at the Material Day.

Check and challenge

- At the inception of the 2017 rating list the Non-Domestic Rating (Alterations of Lists and Appeals) (England) (Amendment) Regulations 2017 introduced changes to the procedure to be adopted by those seeking to alter a rating list entry. The regulations included detailed provisions about who may make a proposal, the grounds on which such a proposal may be made, and what a proposal must contain. They also introduced a preliminary 'check' stage in which facts concerning the property are agreed between the VO and those with the right to make a proposal. The check must be completed before a proposal or 'challenge', to use the words of the regulations, can be submitted.

- In this case the check was submitted by Ms Owen's then retained surveyor Mr Christopher Marriott FRICS. The document was filed electronically on 23 February 2021 and in Section A which is headed 'Why do you want to submit a check?' he ticked the second option which read 'I want to tell the VOA about changes to the property details'. It is worth noting at this point that the sixth option is: 'I want to remove (delete) this property from the rating list. Having ticked the second option Mr Marriott was invited to complete sections G to K. The first question in Section G is: 'is the property part domestic?' and his response was 'no'. He went on to request three changes to the survey details held by the VO in part because he considered part of the Property to be derelict.

- The VO responded on 11 March 2021 and confirmed that they were not going to amend the assessment on the basis of the changes identified. Mr Marriott then moved on to the challenge stage and in Section C of his submission ('Why do you want to challenge your valuation?) he ticked the box headed 'The rateable value shown in the rating list on 1 April 2017 was wrong'. His justification for this assertion was that he wished to inform the VOA of a decision of this Tribunal in relation to a 2010 list appeal on Sandhill Stables at Minehead. Specifically, he submitted that the value of the trotting ring and gallops should be amended.

- In Section K ('Provide a statement why the rating list entry should be altered') Mr Marriott contested the value applied by the VO to the boxes in the main building, identified wooden stables and an arena which he considered beyond economic repair and requested that the trotting ring and gallops should be valued using the methodology adopted by the Tribunal in Hobbs v Gidman (VO) [2017] UKUT 63. The challenge was submitted on 17 March 2021 and sought a revised assessment rateable value £21,250. A valuation at that figure was included in the challenge documentation.

- Ms Owen subsequently decided not to retain the services of Mr Marriott and in August 2022 she sent an e-mail to the VO to explain that 'the property is no longer a commercial premises and the stables/facilities fall in to the curtilage of my domestic home'. She went on to explain that businesses that had operated from the Property were liquidated during the probate process and she had not subsequently traded or run a business at the premises. In her e-mail Ms Owen said that she trained her own horses and kept four retired racehorses. She participated in showing classes, dressage and trail hunting with her horses. Ms Owen stated that the stables were intimately associated with the lodge and water, electricity and sanitation services were shared between the lodge and the equestrian buildings. Muskhill, she concluded, is a single composite hereditament and that in not ticking the box indicating that the Property was domestic, Mr Marriott had 'wrongly administered facts regarding the Property'.

- Further communication between Ms Owen and the VO took place over the next two months and on 10 October 2022 the VO issued its challenge decision. It rejected Mr Marriott's valuation contentions but also dealt with Ms Owen's submission that the Property was domestic and should be deleted from the rating list. The VO noted that a deletion was beyond the scope of the challenge. In its response the VO said that the definition of domestic property for non-domestic rating purposes was to be found in s.66(1) of the Local Government Finance Act 1988 which states:

Domestic property.

(1) Subject to subsections (2), (2B) [F2, (2BB)] and 2E below, property is domestic if

(a) it is used wholly for the purposes of living accommodation,

(b) it is a yard, garden, outhouse or other appurtenance belonging to or enjoyed with property falling within paragraph (a) above,

(c) it is a private garage which either has a floor area of 25 square metres or less or is used wholly or mainly for the accommodation of a private motor vehicle, or

(d) it is private storage premises used wholly or mainly for the storage of articles of domestic use.

They concluded that the stables could not be appurtenant to the domestic dwelling as they pre-existed it and if anything, the domestic dwelling was appurtenant to the stables.

- In Nelson Plant Hire Ltd v Bunyan (VO) [2022] UKUT 309 (LC) the Tribunal (Martin Rodger KC, Deputy President, and Mark Higgin FRICS FIRRV) examined whether it had the jurisdiction to consider a suggested division of the hereditament, having regard to the terms of the appellant's 'challenge' to the entry in the list which simply sought a reduction in the assessment. In that particular case the 'check' referred to a division in assessment.

- At paragraph 65 of the decision the Tribunal said:

'We accept Mr Grant's general proposition that, following the 2017 amendments to the 2009 Regulations, the proposal to alter the list continues to define the scope of any appeal to the VTE or to this Tribunal. The proposal is central to any challenge to the list and the proposition that an appeal could be mounted on a ground which had not been the subject of a proposal is as inconsistent with the structure and language of the 2009 Alteration Regulations in their amended form as it would have been in their original form. Thus, the extent of the disagreement between the parties is framed by the VO's response to a proposal recorded in a decision notice served under regulation 13. The decision notice will record the VO's reasons for concluding that the proposal is not well-founded and will be accompanied by a statement in relation to each of the grounds of the proposal setting out why in the opinion of the VO the ground is not made out, including a summary of any particulars of the grounds of the proposal with which the VO does not agree. The right to appeal to the VTE is triggered by the decision notice (unless no decision is made for a period of 18 months from the date of the proposal). Although the grounds on which an appeal may be made do not themselves refer to the proposal, but only to the fact that the valuation is unreasonable or the list is inaccurate in some other respect, it is clear that the suggested inaccuracy on which the appeal rests must be the same inaccuracy (whether in relation to valuation or otherwise) as prompted the original proposal.

At paragraph 66 the Tribunal noted:

'There is nothing in the 2009 Regulations in their amended form to suggest that it was intended to depart from the long-established position that the scope of any appeal depends on the scope of the proposal. In our judgment the old rule continues to apply'.

- The Tribunal then considered a number of authorities relating to the construction and interpretation of proposals before concluding at paragraph 80 that:

'We are satisfied that it is not necessary for us to reach a conclusion on the material which may be taken into account when interpreting a proposal made in the context of the new check, challenge, appeal process. That is because we agree with the VO's submission that, no matter how much of the material from the check stage is taken into account, it is not possible to interpret the proposal itself as requesting a split of the hereditament. Neither the selected ground ("the rateable value shown in the rating list on 1 April 2017 was wrong"), nor the brief narrative explanation of the challenge refer to the occupation of the Yard by companies other than the appellant or suggest that the list should be altered so that the appellant is not responsible for the whole of the burden of rates.'

- This conclusion is analogous with the facts of the current appeal. At no point in the submission of the 'check' or 'challenge' was the deletion of the Property from the rating list sought. The suggestion that the hereditament is domestic was not raised at all until August 2022 when Ms Owen withdrew Mr Marriott's authority to act and decided to run the case herself.

- The VTE rejected Ms Owen's request for a deletion because it went beyond the scope of the proposal. In my judgment it was correct to do so. The circumstances of this case are even more clear cut than those in Nelson where the check mentioned a division of the assessment. The appeal regulations require the identification of the alteration sought at the outset of the challenge process and options are provided on the form for that very purpose. On the basis of the proposal before me I simply do not have the jurisdiction to consider whether the Property is non-domestic or not. That being the case, I now turn to the valuation of the Property.

Valuation

- Before I consider the valuation and the evidence relating to it, I will deal with Ms Owen's three preliminary contentions regarding the use and marketability of the Property. The first of these was that a hypothetical tenant would not bid for a property that was the subject, at the material day, of litigation relating to probate. I accept the factual basis of this submission but, as a matter of law it is misconceived. The statutory basis of valuation assumes that the hereditament is vacant and that a letting occurs between a hypothetical landlord and tenant on identical terms in every case, thereby ensuring consistency and fairness across all properties. The actual personal circumstances of the occupier are irrelevant and to incorporate them into the assessment would be an anathema to such an approach, and it would be impossible to produce a fair rating list on that basis.

- Ms Owen also submitted that as she was resident in the lodge the Property could not be let as a BHA licenced yard as there would be no means of ensuring that there was a 24 hour presence on site (as required by their regulations), there being no other residential accommodation. As a consequence, the market for the property would be constricted and the property would not therefore command a rent commensurate with a licenced occupation. This argument is again misconceived. The Property is a composite hereditament containing both domestic and non-domestic components (the lodge and the horse racing yard), but the statutory basis of valuation assumes that the whole hereditament is vacant and available for letting, thereby ignoring the occupation of the actual ratepayer. The Property must be valued on the assumption that the lodge is available to be occupied by the owner or the head lad of the yard or another member of staff.

- The final factor said by Ms Owen to have an effect on value was the personal nature of the planning permissions at the Property. Ms McArdle submitted that the local planning authority clearly permitted equine use at the Property and there was a reasonable prospect of continuance. In those circumstances it should be assumed that there was no risk of permission not being granted for the current use once the current occupation had ceased (as must be assumed to have occurred by the material day). She referred to the Lands Tribunal's decision in Oldschool and Oldschool v Coll (VO) (1994) RA/312/1994, where HHJ Rich QC held that the assessment of a house with a personal planning permission for use as offices should be reduced by 2.5% to take account of that condition.

- In Midland Bank plc v Lanham (VO) (1977) 246 EG 1117 the Lands Tribunal (J H Emlyn Jones FRICS) said of the effect of planning restrictions on value:

'Its significance, in my opinion is that the existence of planning restrictions and the necessity of obtaining planning permission for certain changes of use are all factors which affect the minds of potential tenants in the real world and to that extent they must have an influence on value. However the interpretation of these factors remains a matter of evidence and of expert evaluation of evidence.'

- In Rozel Motor Company Limited v Clark (VO) (1983) RA 70 the Lands Tribunal (R C Walmsley FRICS) concluded that:

'As I read the above judgements the critical test is whether or not a particular matter is a characteristic of the hereditament, regardless of who may be its owner or what its owner may intend. Applying this test there seems to be no room for doubt that planning matters are an "essential characteristic" or an "intrinsic circumstance" of a hereditament and accordingly require to be taken into account.'

- The only planning material submitted in this case was copies of planning permissions and correspondence from the Planning Officer. Neither party called a planning expert. There does not seem to have been any attempt to change the existing permissions to allow wider usage and equally no attempt by the planning authority to enforce the terms of the permissions personal to Ms Owen's late partner. The prospective hypothetical tenant would therefore have to judge whether an amended consent would be forthcoming or if there was any likelihood of enforcement action. At the material date only two years had passed since Mr Eddery's death. The rationale behind making the permission personal to him and his family was said by Ms Owen to restrict the intensity of the use of the site. The hypothetical tenant on the other hand, could possibly intend to operate at maximum capacity and might be cautious about the prospects of gaining consent, or the costs of doing so, or the prospect of delay, or any combination of these factors. They would not have the benefit, as we do now, of looking back over the last 8 years and noticing the absence of enforcement.

- The planning circumstances at the Property seem to me to be something that would be in the mind of the hypothetical tenant and would probably lead him or her to temper their bid. In my view the effect is unlikely to be substantial because at the material day the racing yard was established, and I accept Ms McArdle's submission that it could be reasonably anticipated that the use of the areas with personal permission would be allowed to continue. However, at the very least the hypothetical tenant would be faced with the costs, delay and uncertainty associated with an application and I therefore make an allowance of 5%. The hypothetical tenant would take some comfort from the fact that they would occupy under an annual tenancy which could be terminated by them on notice expiring at the end of a year of the tenancy if planning permission for a continuation of the current use could not be obtained.

- Having dispensed with the services of Mr Marriott, Ms Owen did not rely on the evidence of a valuation surveyor. She submitted a report which she headed 'Expert Report' which contained her observations about the site and difficulties she had encountered in occupying it. The respondent called Mr Roy Albert BSc (Hons) MRICS to give expert evidence. He is a technical lead at the Regional Valuation Unit (Wales and West) of the Valuation Office and is based at Bristol. He has specialised in the valuation of equestrian properties since 2021. I now turn to the components of the valuation.

Main Barn

- The Tribunal considered the valuation of racing yards for non-domestic rating purposes in Simon Earle Racing and as in that case it is appropriate to start with the value of the largest of the stable buildings at the Property. Mr Albert concluded that this building was an American Barn, Ms Owen referred to it as the 'Main Barn' and considered the term 'American Barn' a mischaracterisation. The relevance of this distinction is that American Barns are valued for non-domestic rating purposes by adopting the box value or rate from traditional racing yards and then applying a discount of 5%. Ms Owen's argument was that for the barn in question a 5% discount was insufficient.

- In his first report Mr Albert explained that the box 'tone' was location dependent with what he termed 'racing centres' such as Newmarket agreed at £850 to £1,000 per box for the 2017 rating list. He noted that the other principal centres for training are Lambourn in Berkshire and Malton and Middleham in Yorkshire. However, he commented that other areas with numerous training establishments included Epsom in Surrey, Cheltenham, Oxfordshire, Sussex and Wiltshire. He said that box 'tone' in the Midlands was agreed at £550 per box and that this figure had been adopted in the Tribunal's recent decision in Joanne Moore (VO) v Caroline Bailey [2024] UKUT 304 (LC).

- In Simon Earle Racing the starting value was £550 per box. In this case Mr Albert adopted the same approach, starting at £550 per box and applying a reduction of 5%, however, he also made a further discount of 5% for the lack of lighting and poor quality in comparison to the American Barn in the Simon Earle Racing case. That particular building was purpose constructed and had doors built into the external wall of each box to facilitate better ventilation and to increase natural light. Mr Albert's net value was therefore £495 per box. In response to a question from the Tribunal, Mr Albert said that his adopted figure had been arrived at by considering values in surrounding counties and the proximity to other trainers and staff.

- Ms Owen had provided Mr Albert with details of a number of properties that she considered helpful in coming to the appropriate value for the Property. Many of these related to stud farms but four were in respect of licenced yards. Mr Albert helpfully provided details of the assessments from VO records and his personal knowledge in his report, and I set out below the salient points below:

| Address |

Unadjusted box values |

Allowance |

| Yen Hall Farm, West Wratting, Cambridge, CB21 4RX |

£500 per box |

7 boxes have 30% allowance for poor quality

|

| Manor House Farm, Malpas, Cheshire, SY14 8AB |

£550 per box |

20% applied to 21 boxes for poor quality, 10% applied to 20 boxes for poor quality

|

Racing Stables at Yet-Y-Rhug, Letterston, Haverfordwest, Pembrokeshire, SA62 5TB

|

£450 per box |

No allowances |

Hambleton House, Hambleton, Thirsk, North Yorkshire, YO7 2HA

|

£375 per box |

20% allowance for quality of timber boxes |

Unfortunately, no other information beyond the VO's analysis of these assessments was provided. In his evidence Mr Albert also referred (amongst other sites) to:

| Address |

Unadjusted box values |

Comments |

| Sandhill Racing Stables, Bilbrook, Minehead, Somerset TA24 6HA |

£550 per box |

All weather gallop valued at box value less 3% (£530)

|

| Jackdaws Castle, Ford, Temple Guiting, Cheltenham, Glos GL54 5XU |

£630 per box |

2.8 furlong sand trotting ring valued at £300 per furlong

|

| Higher Shutescombe, Charles, Brayford, Barnstaple, Devon EX32 7PU |

£550 per box |

All weather gallops (sand and carpet) valued at box value less 3% (£530) |

Again, no other information, other than the VO's interpretation of the assessment and some undated photographs provided by Ms Owen, was available.

- In replying to questions from the Tribunal Ms Owen confirmed that there were no other licenced yards in the locality, although there were five stud farms within a six mile radius of the Property. She also said that on the occasions when the gallop at the Property were out of action, she had to resort to taking her horses to Kempton Park to exercise them, a distance of some 42 miles. In her view the Property was removed from any racing facilities and the support services which were available in the recognised racing centres.

- In my judgement Buckinghamshire does not seem to a favoured location amongst trainers. It is not in the Midlands and is more than 40 miles south of the former Northamptonshire base of Caroline Bailey Racing. Derivation of a value from the tone in neighbouring counties, which was the approach in Simon Earle Racing is more challenging at the Property. In that case the property was in Wiltshire where there was no established tone but was relatively close to yards in adjacent counties. That does not appear to be the case at the Property.

- The assessments at Yell Hall Farm and Hambleton which are respectively 10 miles from Newmarket and just over 20 miles from Malton, suggest that even where yards are close to leading training centres values can be considerably lower than the levels that prevail in those locations. Taking all of the locational aspects into account I have come to the view that the value should be lower than the Midlands tone. I note that other locations can have values as low as £375 per box but in my view being located in Buckinghamshire is less of a disadvantage than being in rural South Wales where the prevailing value is £450 per box. Adjusting the Midlands tone by 10% results in a figure of £495 per box and I adopt that figure.

- Turning to the building itself the conclusion I have reached is that the Main Barn is a hybrid, it shares some features with a purpose built American Barn but its agricultural origins leave it rather compromised in comparison. It follows that when starting from a value for a standard box, the Main Barn warrants a larger reduction than the 5% used for a purpose built American barn. My judgement is that the box value should be reduced by 7.5% for the hybrid nature of the building and I adopt Mr Albert's allowance of a further 5% for lack of daylight. The combined effect of these allowances is that the box value is reduced to £433.13, which I round to £433.00.

- The Main Barn contains a number of ancillary rooms including a tack room, a feed store and an office. These are considered essential for the operation of a racing yard and are reflected in the box value. In this particular case there are two further rooms; a storeroom used by Ms Owen for her personal effects and a mess room. Mr Albert included the storeroom in the domestic element of the assessment, and it is therefore disregarded for non-domestic rating purposes. Mr Albert considered that the mess room was not essential to the operation of the yard and had valued it at £15 per m2 resulting to a figure of £303 in rateable value terms. I disagree with his approach; the hypothetical tenant might use the yard more intensively than Ms Owen and space for staff to take a break and prepare food and drink would be needed. It should therefore be reflected in the box value.

- The remaining aspect of the Main Barn that requires consideration is the horse walker and the space it occupies. Ms Owen said that the horse walker dated from 1986 and that one of the compartments was unserviceable. It was said to be impossible to obtain parts as the manufacturer was no longer in business. Mr Albert asserted that that it should be valued as a fully functioning, five compartment machine. He adopted the agreed scale of £50 per compartment. The rateable part of the horse walker is the concrete base, rather than the rotating machinery. The value is derived from the cost of the base and consequently a base capable of accommodating five horses is more valuable than a smaller four horse base. At the property the walker is installed on the barn floor and Mr Albert had added 100 m2 of barn space at £3 per m2 for the area in which it was located. On my inspection it was not apparent that any works had taken place to adapt the barn floor to make it suitable for the walker. Although the sums involved are not particularly consequential there seems to be an element of double counting in Mr Albert's approach. In Simon Earle Racing the horse walker was located outside the barn (as seems to be the usual practice) and was enclosed. It was valued at £50 per compartment but the design incorporated a 255 m2 lunge ring which was valued at £4 per m2. I have no doubt that the arrangement at the Property is inferior, notwithstanding that the horse walker is indoors. It seems to me that in the circumstances the correct approach is to value the building but not the base separately as the value of the floor is incorporated in the value of the building. I therefore adopt a value of £300.

Other boxes

- At the material day there were 15 other boxes at the Property which were not in racing use. These were in various locations and included larger boxes used for foaling mares:

At the rear of the hay barn 4 standard boxes, 1 large box

In the stud barn 7 standard boxes, 1 large box

Timber boxes next to stud barn one standard box, 1 large box.

- By the time of the hearing the hay barn boxes and the large box in the stud barn had been removed. An additional five timber boxes were in a state of disrepair at the time of my inspection but were included in the Council Tax assessment. Ms Owen took the view that domestic boxes should be those nearer the Lodge, namely boxes inside the Main Barn. This would have the effect of taking the more valuable boxes out of the rating assessment. I take the view that Mr Albert's approach is correct, the five timber boxes, notwithstanding their condition, are akin to the type of box one would associate with a domestic property. They properly belong in the Council Tax assessment. That being the case there is no need to consider the impact of their condition on the assessment. The two timber boxes adjacent to the stud barn are in my view superior in specification and condition to the other five. Mr Albert submitted that for the purposes of the 2017 List the unadjusted value for boxes not used for racing purposes is established by agreement at £350 per box. The larger boxes are valued at £385 per box. I therefore adopt these respective figures.

The arena

- Ms Owen submitted that at the material day the clay sub-base of the arena had heaved and as a consequence it was both incapable of beneficial occupation and at the end of its economic life. She explained that the arena was badly constructed and lacked drainage. It had been built deep into the ground and was consequently prone to flooding. It was originally built for Mr Eddery's children to use rather than as a facility for racehorses. The Carter Jonas report noted that 'the lining of the all-weather arena had failed and large stones have surfaced throughout'. At the time of my inspection, the arena was very wet and muddy, especially at the southern end, although I am mindful that my visit took place seven years after the material day. Ms Owen said that she made occasional use of the arena for the turnout of retired racehorse when she needed to limit their consumption of grass. Mr Albert included in his evidence a Google Earth photograph which showed the arena being used for this purpose. A report dated May 2023 by Martin Collins Enterprises who describe themselves as 'setting the winning standard in equine surfaces' concluded that it would be cheaper to replace the arena than repair it. Their 2023 costings amounted to £111,291.20 for refurbishment and £79,030.00 for a newly constructed arena.

- Mr Albert acknowledged in his report that the arena was in a state of disrepair. It was originally included in the assessment at £1.50 per m2. He had inspected the property for the first time in May 2024 and he confirmed that no one from the VO had inspected the Property between May 2009 and January 2022. In assessing the condition of the arena at the material day he relied on a photograph from the Carter Jonas report taken in May 2016 and concluded that it had deteriorated since that date. He had obtained detailed costings from VO building surveyors who concluded that the cost at the antecedent valuation date ('AVD') of refurbishing the arena would be £75,550.16 and a replacement would amount to £53,649.61. He drew a comparison with the arena at Sheepcote Arena, Barterstree, Hereford HR1 4DE, which was situated on a stud farm and equestrian centre. This arena was built on the site of an old tennis court and lacked proper drainage. It too had a propensity to flood with a consequent limitation on usage. It had been agreed at £1 per m2 and this was the rate Mr Albert adopted at the Property. His rationale for this position was that an arena was not essential for the training of racehorses and the hypothetical landlord would not entertain the outlay on repairs but would accept a lower value instead.

- The VTE noted in its decision that it had no evidence of costs showing repair to be uneconomic at the material day, but limited use was ongoing, and Mr Marriott had proposed a rate of £0.75 per m2 in his challenge valuation. The VTE also had the Sheepcote evidence to consider and concluded that the arena at that property was superior to its counterpart at the Property. It too relied on photographic evidence and decided that a rate of £0.75 per m2 was appropriate although it did not set out its detailed methodology in coming to that figure.

- It is clear that the arena was not built to the highest standards and currently requires significant remediation. It is not possible to be definitive about its condition at the material day; the only evidence is a single line of commentary together with a rather grainy photograph in a report from 2016, and a Google Earth image showing it in use. There is no evidence of flooding in either photograph but as stones were emerging it is reasonable to conclude that the liner had been breached. Bearing in mind that it was originally constructed for a purpose unrelated to the use of the Property as a racing yard I agree with Mr Albert that it is unlikely that the hypothetical landlord would, at the material day, consider it worthwhile to repair it. It was being used for turn out at that point and that remains the case today. Photographs of the Sheepcote arena submitted in evidence and dated 2014 show it to be superior to the arena in this case. I have therefore come to the view that the arena at the Property has a modicum of value and the 25% discount to the £1 per m2 Sheepcote rate, as adopted by the VTE is the correct approach on the assumption that the arena was unrepaired.

The trotting ring

- Ms Owen confirmed in her evidence that the trotting ring extended to 293 metres (1.45 furlongs) in length and had a width of 3 metres. It has a sand base with a rubber and carpet fibre topping. The planning permission for its construction was personal to Mr Eddery. It was said to have flooded and frozen in the winter of 2022/23 but there is no record of its condition in 2017 or evidence that drainage issues had arisen earlier. Mr Albert had adopted an approach to the valuation derived from the Tribunal's decision in Hobbs v Gidman (VO) which used the unadjusted box rate less 3%, or putting it another way, £530 per furlong. This resulted in a figure of £768. Martin Collins suggested in their report that the ring would benefit from the installation of a 'cut off drain', the cost of which was quoted at £5,787.60 plus VAT. I see no reason to depart from Mr Albert's methodology but having determined an unadjusted box rate of £495 per box the rate per furlong drops to £480. I will return to the question of remedial works when I deal with the gallop.

The gallop

- Although the value attached to the gallop is not a particularly significant element in the assessment, it proved to be the most contentious component. The List entry includes a figure of £3,339 which was based on the same approach as the trotting ring of the unadjusted box rate less 3% per furlong. This was the figure adopted by Mr Albert. Ms Owen said that the gallop was built in 2004 and the planning permission was again personal to Mr Eddery. In her view at the material day the gallop was incapable of beneficial occupation and the planning constraints would prevent the property being let in the open market. Ms Owen also submitted that the gallop has been beset with problems since it was installed. In particular it was built into the ground with a tarmac base and no drainage. On my inspection I noted that it appeared to be built in a channel with the banks and pasture either side higher than the riding surface. Ms Owen said it acted like a drain and at the time of my visit rainwater had washed the surface downhill creating gullies in the surface and making it unsafe to ride on. In addition, a small river adjacent to the turning circle at the northern end of the gallop has a tendency to flood. Taken together these various problems meant that Ms Owen could only reliably use the two furlongs at the top of the gallop. She submitted a number of photographs depicting the problems and her efforts using farm machinery to try to restore the surface.

- The Carter Jonas report commented that:

'The gallop and trotting ring appear to be well maintained and fit for purpose.'

However, Ms Owen included as part of her evidence a report by McArdle Equestrian Surfaces dated 22 July 2009 following a visit to the site by their Director and Head of Operations. They found that there had been a catastrophic failure of the drainage system on the flat, northern part of the gallop, where the central drain had been forced up through the sub base and tarmac separation layer. The failure had resulted from a number of factors including:

1) The central drain being insufficient in diameter

2) There were no drainage outfalls to take the water away from the gallop

3) The central drain was full of clay/subsoil and should have been laid in a trench and surrounded by stone and a geotextile membrane

4) The stone layer was oolitic limestone which was not suitable

5) The stone layer was of insufficient depth

6) The tarmac layer was of insufficient depth

McArdle suggested a 12 day programme of works including a new drainage system and the laying of a new base for the gallop. The existing Parkway Eurotrac surface would be salvaged and used again with the necessary top up to bring it to the required depth. The cost of these works would amount to £34,938.24 including VAT. It is not known whether any of these works were undertaken but given the current condition it seems unlikely. When Martin Collins Enterprises reported on the gallop in 2023 they found the same oolitic limestone base. They too suggested a revised drainage system involving 1,269 metres of 'cut off' drains. Their solution was priced at £51,059.48 including VAT. They also suggested that the turning circle be relocated approximately 250 metres south of its existing position and that a new raised 12 metre diameter circle be constructed. This element was priced at £15,573.31 including VAT.

- Mr Albert commissioned the building surveying team at the VOA to rebase the Martin Collins costs to 1 April 2017 and the resultant figures were £28,884.83 and £11,277.59 respectively. Mr Albert referred in his evidence to the Tribunal's decision in Thomas & Davies (Merthyr Tydfil) Ltd v Denly (VO) [2014] UKUT 146 (LC) (N J Rose FRICS). In that case the costs of works amounted to £442,431 at the AVD or 5.64 times the rateable value. The Tribunal found that the hypothetical landlord would have undertaken the works and in fact they were completed by the actual occupier after the material day. In this case Mr Albert aggregated the trotting ring works and those for the gallop to produce a figure of £44,091.34 or 2.2 times the existing assessment. He concluded that the hypothetical landlord would consider these works economic to undertake and therefore made no adjustment to the valuation of the gallop or trotting ring. There is no evidence that at the material day the trotting ring was in any way unusable and in my view there is no need to take account of the expenditure suggested by Martin Collins.

- Otherwise, I agree with Mr Albert's conclusion. The cost of putting the gallop into repair is something that the hypothetical landlord would, in my view, consider to be an economic proposition. This would remain the case even adopting the lower values I have arrived at. It is a stipulation of BHA licencing that the trainer should have access to a gallop and since there are no others in the locality it would be essential for the gallop to be put back into repair to achieve the hypothetical letting. I note that in Thomas and Davies the works were judged by the Tribunal to be repairs even though the result of the project would be an improvement over what preceded it. They replaced items that were dilapidated and beyond repair. I do not regard the proposed works at the gallop as an improvement, they seem to me to be the minimum required to enable the gallop to function in the manner intended. They would however result in a materially shorter gallop and I take account of this factor in the valuation which follows below.

End allowances

- It is agreed between the parties that the footpath that crosses the Property is a disability and that an allowance of 5% is appropriate.

- It was apparent from my site visit that the topography of the site is such that there are at various points in the yard where there are significant slopes. Ms Owen confirmed at the hearing that these were undesirable from a training perspective and caused issues with drainage. Ms Owen sought an allowance of 5% for this factor, however I consider that an allowance of 2.5% is appropriate for this disability.

- I have provided my conclusion regarding the effect on value of personal planning permissions earlier in this decision.

- Ms Owen submitted that the entrance into the property was shared with the neighbouring Musk Hill Farmhouse (previously part of the Property) and that this arrangement warranted an allowance of 5%. I disagree. The volume of traffic visiting the Property, or the Farmhouse is unlikely to be such that it will inconvenience either occupier.

- The final component of the valuation is stud farms relief. Parliament has legislated for partial rate relief from the payment of rates for farmers who also breed horses and ponies, by enacting Paragraph 2A.- (1) of Schedule 6 to the Local Government Finance Act 1988 (inserted by paragraph 38(11) of Schedule 5 to the Local Government & Housing Act 1989). This takes the form of a reduction in rateable value. Ms Owen confirmed at the hearing that at the material day she was breeding horses and it was agreed between the parties that stud farm relief should apply. Mr Albert had calculated a deduction of rateable value £4,655 as being appropriate in the circumstances and I therefore adopt that figure.

Decision

- The appeal is determined at rateable value £15,600. My valuation is appended to this decision.

Mark Higgin FRICS FIRRV

Member

12 February 2025

Right of appeal

Any party has a right of appeal to the Court of Appeal on any point of law arising from this decision. The right of appeal may be exercised only with permission. An application for permission to appeal to the Court of Appeal must be sent or delivered to the Tribunal so that it is received within 1 month after the date on which this decision is sent to the parties (unless an application for costs is made within 14 days of the decision being sent to the parties, in which case an application for permission to appeal must be made within 1 month of the date on which the Tribunal's decision on costs is sent to the parties). An application for permission to appeal must identify the decision of the Tribunal to which it relates, identify the alleged error or errors of law in the decision, and state the result the party making the application is seeking. If the Tribunal refuses permission to appeal a further application may then be made to the Court of Appeal for permission.

| Musk Hill Farm, Nether Winchendon, Aylesbury, Buckinghamshire, HP18 OEB |

| Item |

|

No/unit |

Rate £/m2 |

Total |

| Racing boxes |

|

31 |

£ 433 |

£ 13,423 |

| Non racing boxes |

|

12 |

£ 350 |

£ 4,200 |

| Large non racing boxes |

|

3 |

£ 385 |

£ 1,155 |

| Horse walker building (m2) |

|

100 |

£ 3 |

£ 300 |

| |

|

|

|

|

| Arena (m2) |

|

1220 |

£ 0.75 |

£ 915 |

| Gallop (Furlongs) |

|

5.2 |

£ 480 |

£ 2,496 |

| Trotting ring (Furlongs) |

|

1.45 |

£ 480 |

£ 696 |

| |

|

|

|

£ 23,185 |

| |

|

|

|

|

| Less for footpath |

|

|

-5.0% |

-£ 1,159 |

| Less for adverse topography |

|

|

-2.5% |

-£ 580 |

| Less for planning issues |

|

|

-5.0% |

-£ 1,159 |

| |

|

|

|

£ 20,287 |

| |

|

|

|

|

| Less Stud Relief |

|

|

|

-£ 4,655 |

| |

|

|

|

|

| |

|

|

Total |

£ 15,632 |

| |

|

|

|

|

| |

|

|

Say |

£ 15,600 |